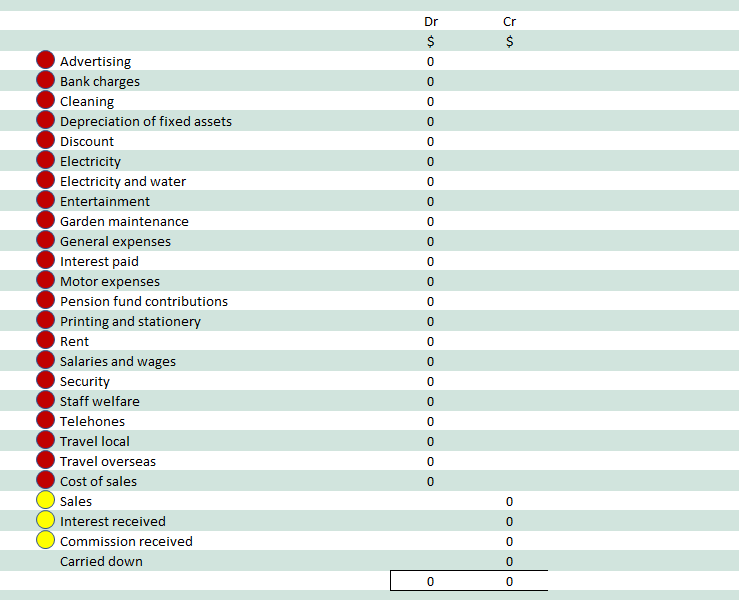

Chart of Accounts

Colour coded to assist with identifying whether a debit or credit item is an item of expense or income, or is an asset or liability item.

We usually draw a chart of accounts so that we can allocate the expense and income items to certain pre-determined general ledger accounts. Each business and industry usually has its own commonly defined income and expense categories and terms. Some generate sales, others fees, commission, rental income, interest etc.

We now need to understand the debit and credit system of accounting.

Expenses are debit entries

Income as a credit entry

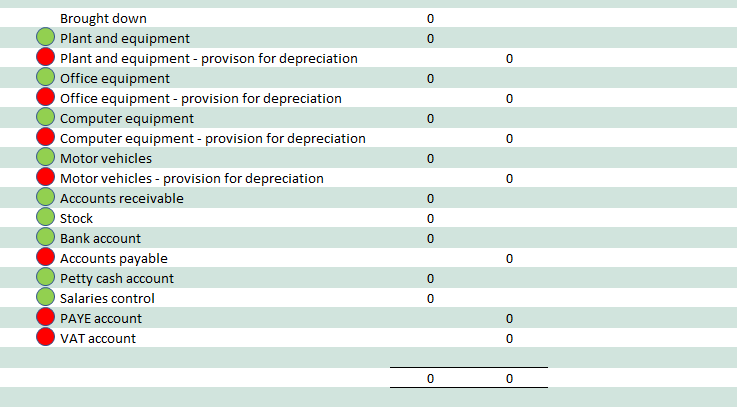

Assets are debit entries

Liabilities are credit entries

Most trial balances are set up so that the income and expense items appear in the top half of the trial balance. The assets and liabilities appear in the bottom half of the trial balance.

The difference between the debits and credits in the top half of the trial balance are equal to, but opposite the difference between the assets and liabilities in the bottom half of the trial balance.

The income and expenditure section of the trial balance reflects a summary of the movements in the asset and liability section. For example we have twelve monthly rental payments and in the trial balance we show those twelve monthly payments as one amount for the year. The twelve payments are first entered into the general ledger and the total entered into the trial balance.

The colours below are used on the chart of accounts to assist with the allocation of the receipt or payment : –

The above chart of accounts can be expanded or reduced according to the needs of the business entity. It helps with identifying whether the expenditure item relates to income or expenditure or to an asset or liability account.

The fixed assets are recorded at cost when originally purchased. As they are used their value decreases due to wear and tear. Also they become antiquated and are replaced by more efficient better designed equipment. Businesses are required to reduce the value of the assets to keep in line with the reducing value of the equipment and a charge is made for this reduction called depreciation.

This is a non cash entry between the “Depreciation account” which is a debit entry expense account and the “Provision for depreciation” which is a suspense liability account which is the reduction in the value of the asset being depreciated.

Depreciation is an estimated expense so the estimated accumulating depreciation is held in suspense in the relevant “Provision for depreciation account” until the asset is finally disposed of and the final difference between the original cost and the proceeds received are determined and the loss or profit and accumulated depreciation and original cost are adjusted and the final result recorded in the books of account.

Companies are required to keep an asset register in which each asset is recorded and the totals of each asset class agreed to the totals of each asset class in the books of account. The total of the depreciation on each asset class is totalled in the asset register at the end of each year and agreed to the total of the “Provision for depreciation account” for that relevant class of asset in the books of account.