Single entry system of accounting

The double entry system of accounting is used where detailed trading records are required for the purpose of determining the taxable trading income of a business enterprise.

The simple process of totalling all the assets of a business and then deducting the gross liabilities from that total would give you the net asset value at the year end date. One would then deduct the net asset value of the business at the beginning of the year to arrive at the net profit or loss for the year. This system of accounting would suffice in a country where no taxation is payable and there are a limited number of owners.

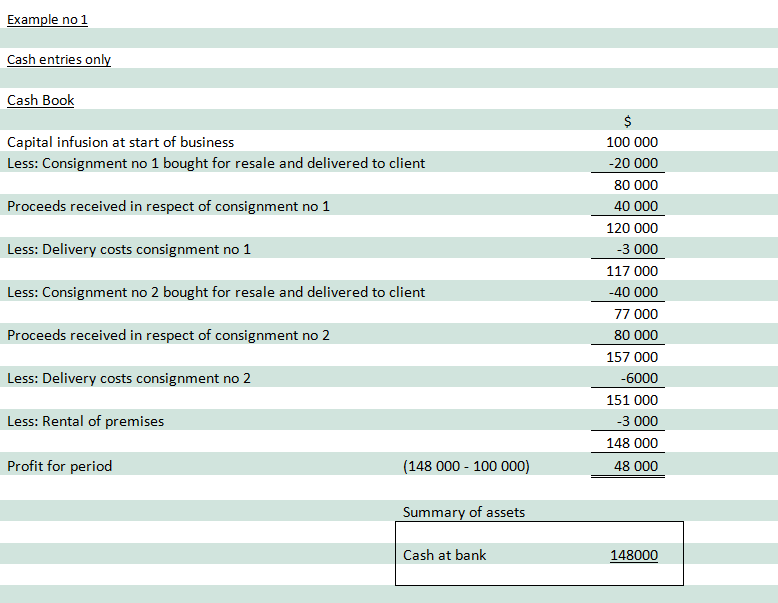

A simple cash in and cash out business with no other assets and liabilities would give you an accurate record of your profit for the year. Any increase in the cash balance over the balance at the beginning of the year would be the profit and a decrease would give you a loss.

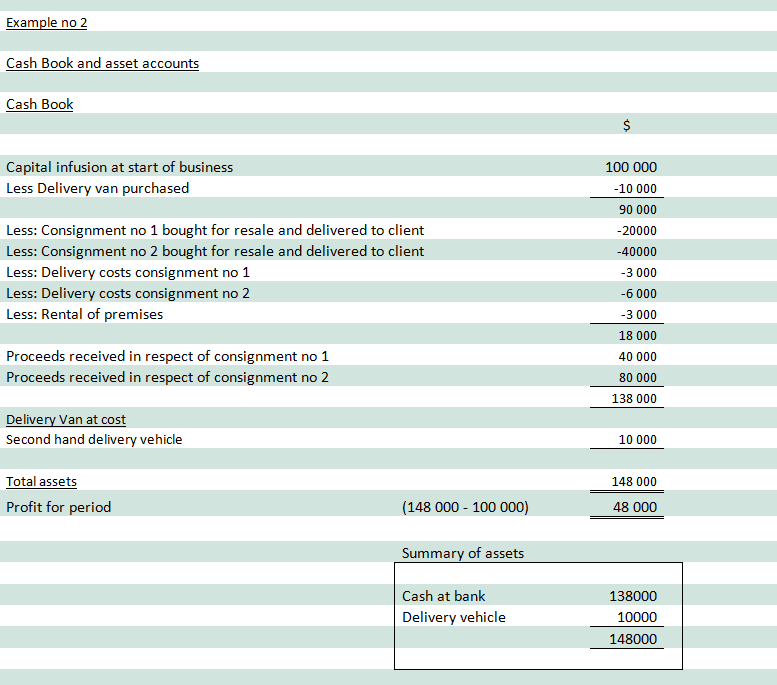

This system could be expanded by only recording the double entry when asset and liability movements are involved. Also only recording the liability side of the entry when consumable goods are bought on credit.

Example 1 of Single Entry System

_______________________________________

Example 2 of Single Entry System

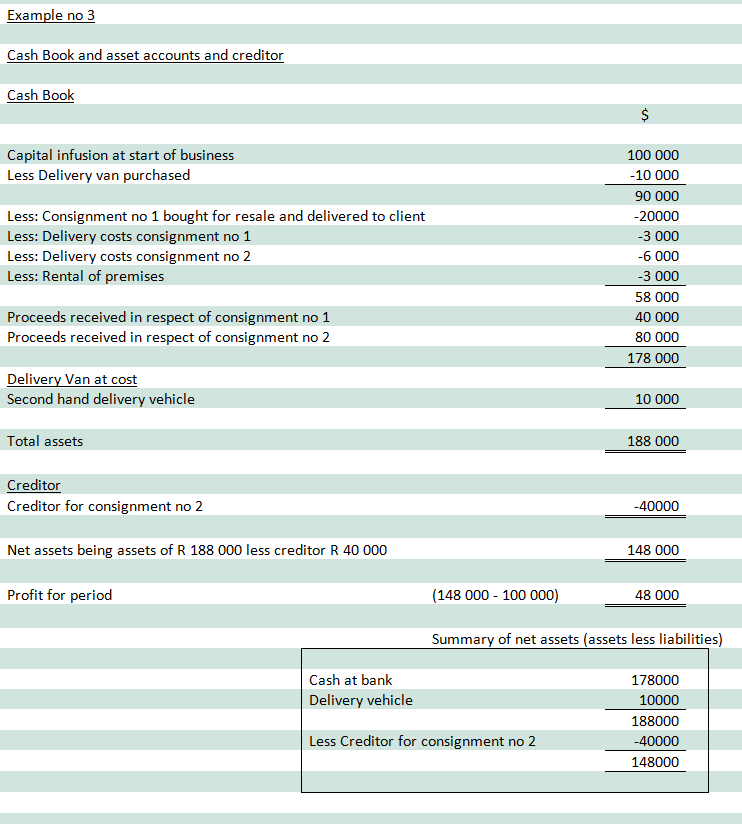

The scenario can alter for all sorts of reasons. For example, if the supplier of the second consignment granted us 60 days to pay for the consignment and the purchaser paid us in 30 days. However, the payment was not due at the year end. Then there would be an additional forty thousand rand in the bank and a creditor for forty thousand rand.

The profit will not alter provided we have compensating factors. In the case of the unpaid creditor the goods were received before the year end. If we increase the creditor by forty thousand rand, we also increase the bank balance by the same amount.

This is evident from the next example

Now we need to look at the benefit of applying the double entry system to the single entry scenario. Which is shown in our example above.

I have designed a colour coded chart of accounts to assist the learner in identifying the general ledger account. Using this will allow you to become familiar with which payment or receipt item needs to be allocated.

As we progress the learner will refer less and less to the chart of accounts.

This is more broadly explained in the Chart of Accounts section.

We now need to understand the debit and credit system of accounting.