Deferred Taxation

Deferred taxation arises when the book value of assets and liabilities is different from the taxation value and this is usually the case in the initial years of trading.

The depreciation of fixed assets over their useful productive lives has long been recognised by the accounting fraternity. Revenue authorities of most countries have recognised this principle and usually have fixed rates of depreciation for the various asset classes. The depreciation rates are referred to as capital allowances or wear and tear allowances or some similar wording according to the terminology used in the tax law as enacted in the various countries.

The revenue authorities usually specify a fixed rate based on the original cost of the specific asset class until the value has been reduced to say one dollar or pound or the specific currency in use in the country concerned. The revenue authorities usually make provision for an asset register to be maintained in order that the value of the asset is recouped on disposal of the asset. In addition to the normal capital and wear and tear rates of depreciation the revenue authorities may also grant higher rates in certain areas of the country where they wish to encourage the development of industry and commercial activity for the purpose of job creation and reducing overcrowding in other areas of the country.

Prescribed allowances

The rates of capital allowances and wear and tear allowances prescribed by the revenue authorities do not usually provide for some residual valuation and the accounting fraternity have recognised that the disparity in the rates adopted by the various companies in their financial records and the rates claimed for taxation purposes result in the profits being a lot higher in the initial years than the years after the tax benefits have been exhausted.

To prevent the profits being distributed more generously to shareholders in the early years and then being withheld in the later years due to an increase in the taxation charge due to the lower capital allowances and wear and tear allowances, the principle of raising a tax charge on the disparity in the allowances is generally adopted. This charge is known as deferred taxation since it is providing for the amount of taxation that would have been paid but for the allowances, and then deferring it to a future date.

When calculating the deferred tax amount to be raised, list the tax value of the assets and liabilities. Where the allowances differ from the book value apply the tax rate to the difference. Deduct this amount from the profits for the year and credit this amount to a deferred tax account. Where the tax is higher due to income being taxed in advance as is the case sometimes with advance deposits then the tax paid in advance is deducted from the current tax charge and carried forward to the next year as taxation paid in advance.

Example no 1

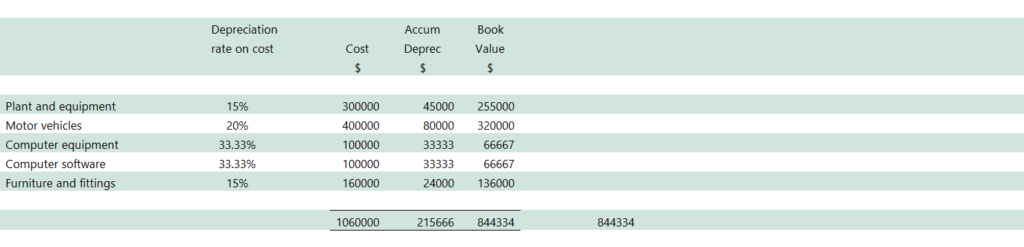

The book value of fixed assets at the end of the first year of trading is as below: –

These are the amounts as they would appear in the financial statements. These values would have been extracted from the fixed asset register

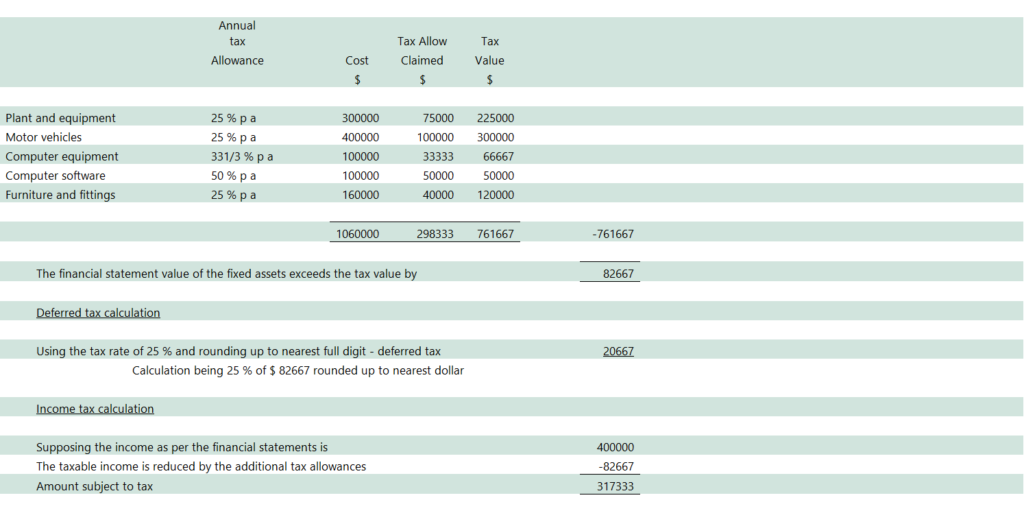

The tax value of the fixed assets at the end of the first year of trading is as below: –

A separate asset register would be kept showing the tax value of the assets

Important to note

The tax that is shown in the Income Statement is the exact percentage of the profit according to the official tax rate. This is the tax as calculated plus the deferred tax.

The only time this varies is when there are fines or other non-allowable expense items included in the Income Statement. Once the capital allowances or wear and tear allowances have been exhausted. Then the tax payable will be more than the amount calculated directly from the income statement, but the difference will be debited to the deferred taxation account thereby reducing this account.

Example no 2

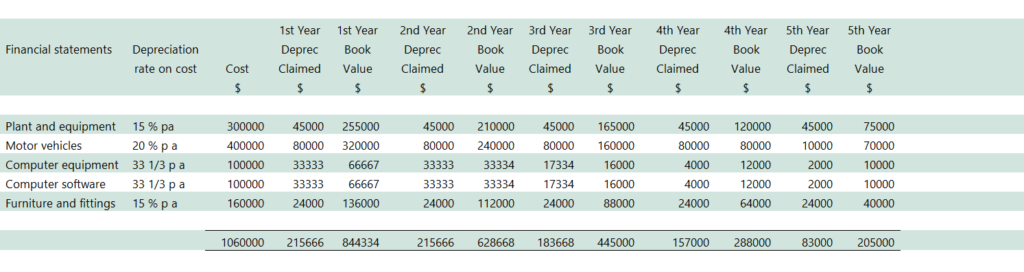

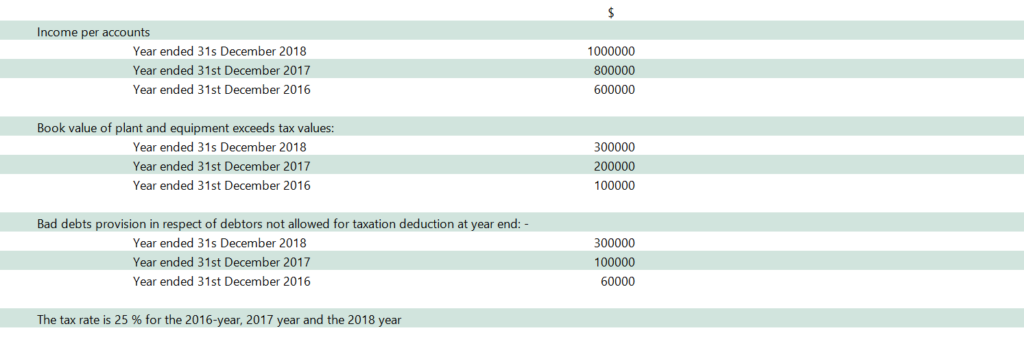

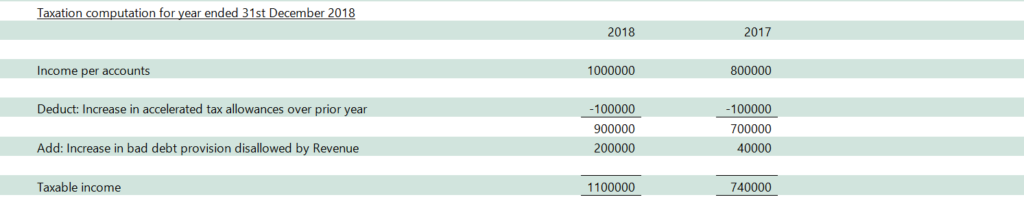

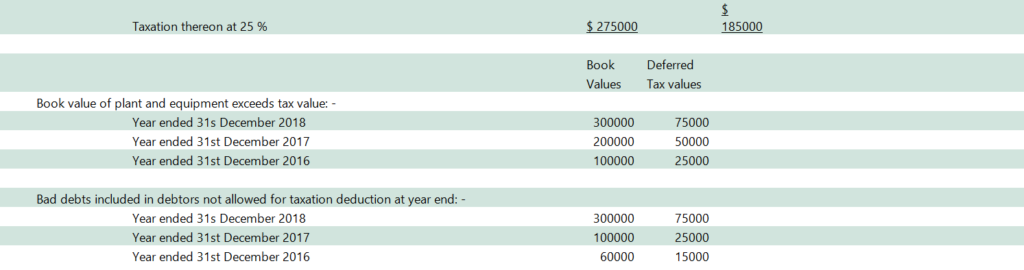

This is a summary of the first five years of the depreciation claimed in the financial statements and the allowances claimed for taxation purpose and the change from the tax benefit to the tax liability will be obvious in respect of the accelerated tax claims.

The accounting value of the fixed assets for the first five years of trading are as below:-

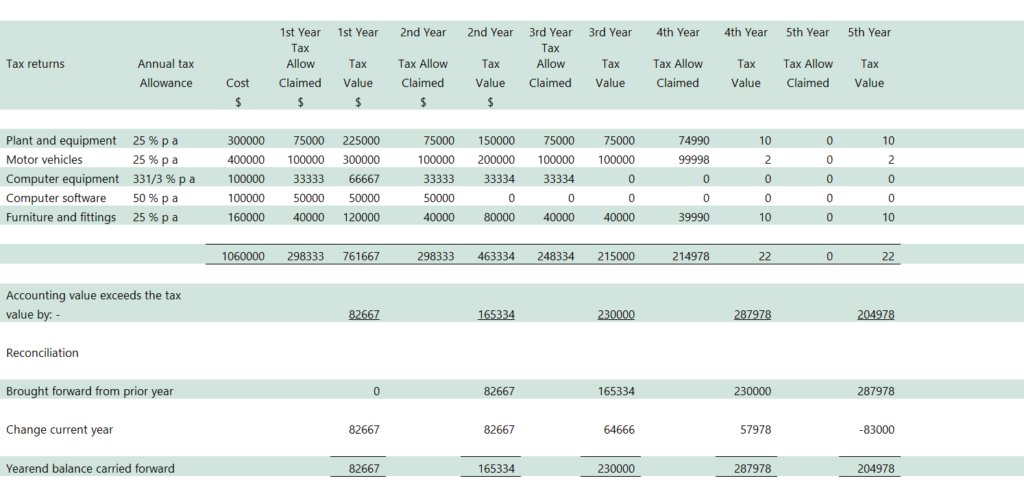

The tax value of the fixed assets for the first five years are as below:-

Important to note

The deferred tax provision increases for five years. Then from the fifth year the provision is reduced as the book values are reduced by depreciation provided in the financial statements as the possible disposal values are reduced. No disposal value is accorded to computers. These are generally out of date after three years and impossible to find an interested purchaser. Also they may have confidential information stored and so it is easier to store the old computers in a safe place.

The value of the fixed assets will gradually decrease in value going forward until such time they are sold or discarded.

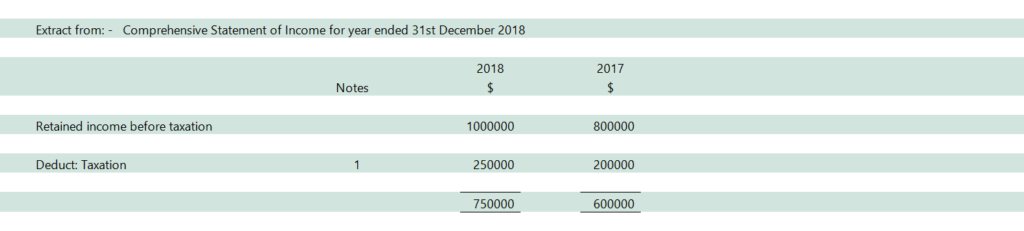

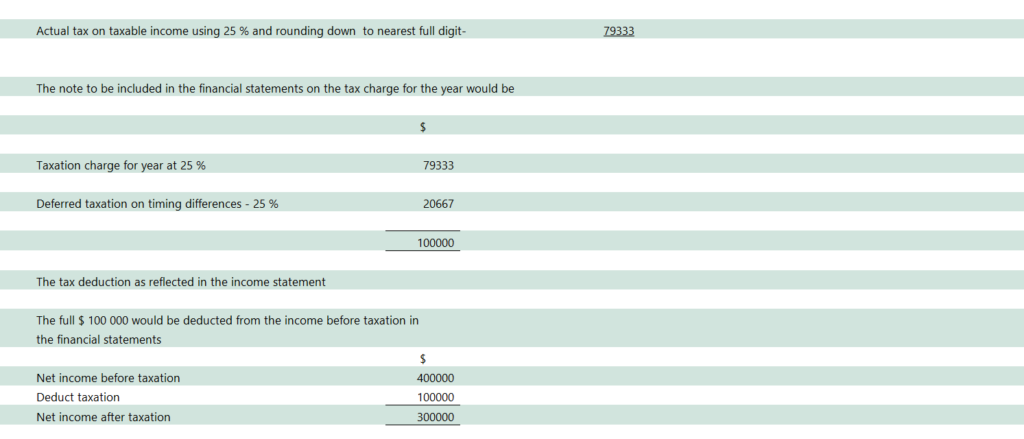

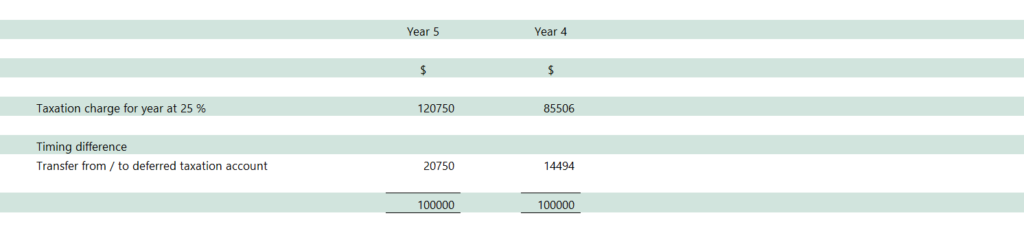

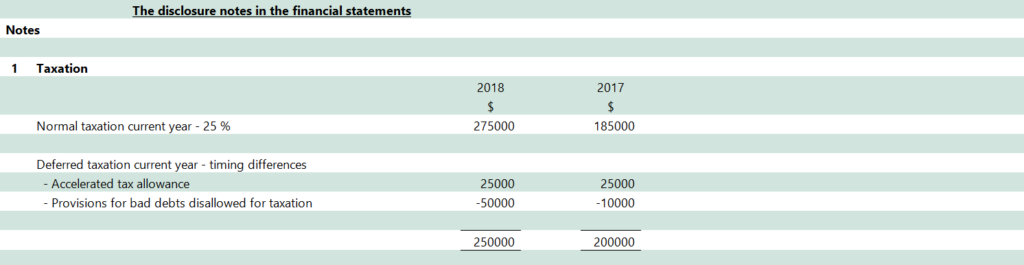

The note to be included in the financial statements on the tax charge for the year would be

The tax deduction as reflected in the income statement

The full $ 100 000 would be deducted from the income before taxation in the financial statements

In the balance sheet you would show the following under current liabilities

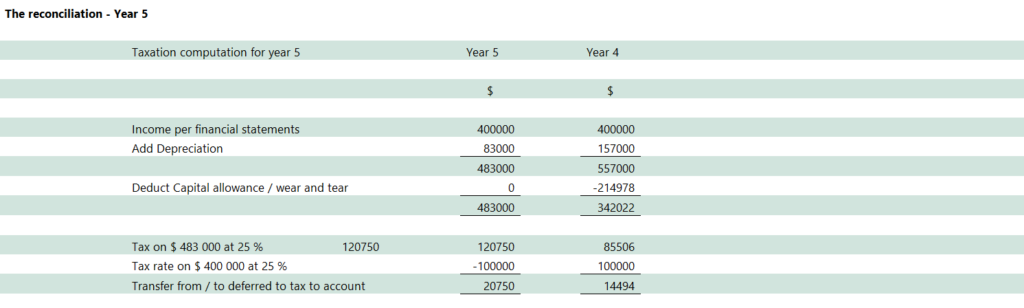

In the reconciliation of the deferred taxation account, you can clearly see where the cross cast from year 1 to year 4 totals $ 71 995 and then the reversal of $ 20 750 reduces this balance to $ 51 245. This is verified by applying the tax rate of 25 % to the amount of $ 204 978 being the excess of the book value of the assets over tax values at the end of year 5.

To comply with IFRS we would need to show the movement on the deferred taxation account. Since we are more interested in the arithmetical calculations and the correctness of the balancing and reconciliation of the financial statements we will deal with this at a later stage.

General note on deferred taxation

The Revenue services over the years have arrived at certain rules to prevent taxpayers making false tax deduction claims and some of these which apply in some countries but not in other countries: –

Excessive provisions where the expense is incurred and invoiced to the business in the following year and is therefore disallowed. An exception would be where the tax act may provide for the deduction of such expenditure such as goods bought after the year end in respect of invoices raised in the prior year and included in the income for that year.

Payments in advance which are allowed since the money has been outlaid.

Advance receipts from debtors where these amounts are taxed in the year of receipt, here the revenue usually allow a deduction especially if it is in respect of goods still to be supplied. (This is to prevent the non-invoicing of income earned in one year being rolled forward into the following year.)

Provisions for bad debts where the revenue services may only allow say 25 % or 50 % of the provision.

Important to note

In the above cases the expense is disallowed in the year it is claimed. It is allowed in the year the expense is incurred. The reversal of the provision is allowed if the original claim is not allowed.

Certain countries do not allow deductions of entertainment expenses especially if food and drink are involved.

Others do not allow the deduction of traffic fines and other fines as these are not considered to be an expense in the production of income.

Where certain provisions are made in one year for accounting purposes and the accountant is aware that these will not be allowed for taxation then the prudent course of action is not to claim this amount for taxation purposes, but provide for deferred taxation on those amounts to keep the books in line with the taxation liability. Advance payments would also be included in the taxable income calculation for the current year but claimed as a deduction in the following year.

A provision is an estimate of expenditure to be incurred at some time in the future. It is made to reduce the profits available for distribution in a current period to provide for such expenditure should it occur.

NB. Regarding any examples in this website, it will be stated as to the possible tax treatment to be applied. It is impossible to provide for different tax jurisdictions throughout the world and the reader needs to refer to the specific tax laws in their own country when writing examinations and dealing with tax authorities in their own jurisdiction.

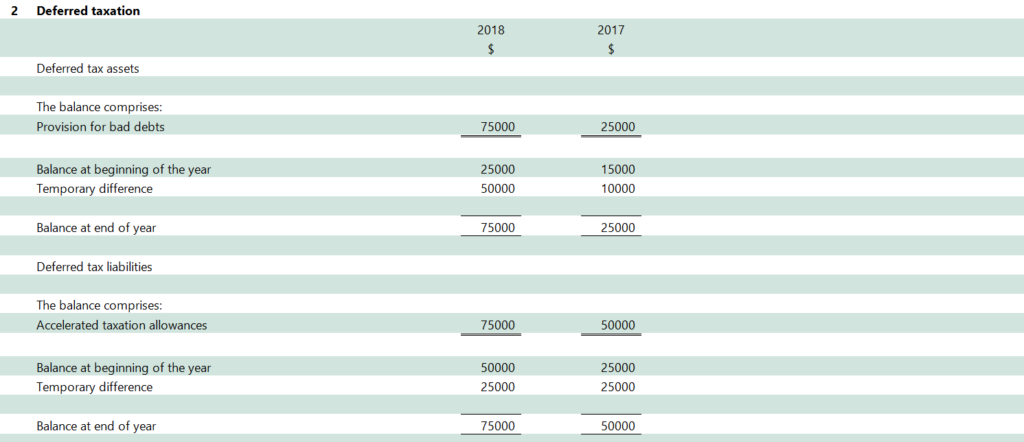

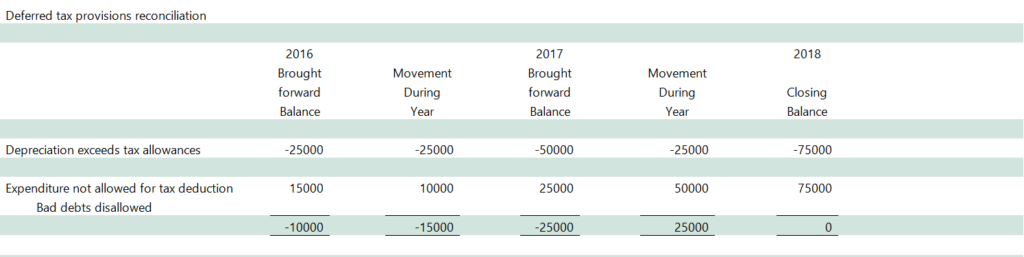

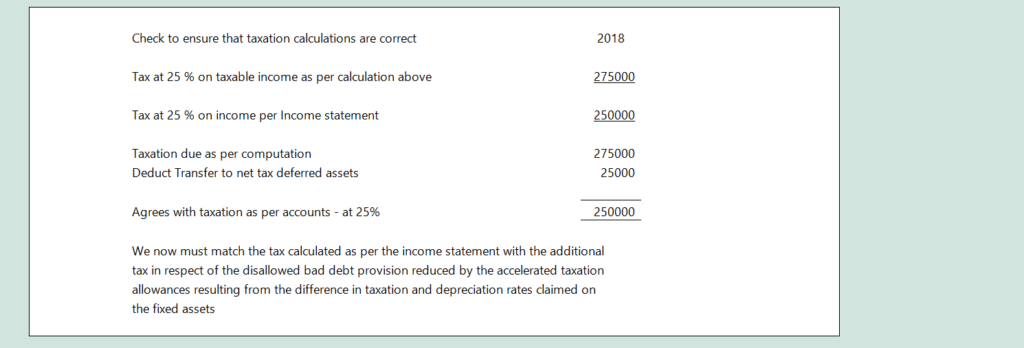

Example no 3

The calculation and reconciliation of the deferred taxation provision can be very time consuming and mind blowing and when there is more than one expense or income type. It is a very good idea to use a spreadsheet. Then reflect the balances brought forward in the first column, the movement in the second column, and the final balance in the right-hand column.

In the example below the following applies: –

NB The entry in the “Comprehensive Statement of Income” is the opposite to the entry raising the deferred tax liability or asset. It is the movement that is reflected in the reconciliation working that is shown in the taxation note to the income statement and it is the closing balance that is reflected in the balance sheet or “Statement of financial position” as it is now known.