Moving on to the double entry system

Looking carefully at the three examples it is obvious that if we record the other leg of the single entry systematically, then as the transactions unfold then we will have an updated record of our business transactions. We will know exactly how much profit we have made and how much stock we have on hand. Also how much is owed to us and by us to our creditors.

In our next example the first entry is a deposit of $ 100 000 into the bank account. The responding entry is a credit to the capital account of the owner of the business.

Assets are recorded as debits and liabilities are recorded as credits.

Expenses are also recorded as debits and in this instance the credit goes to reduce the bank account balance. A simple rule would be if a cash payment relates to an expense it would convert the bank asset debit to an expense debit. When buying another asset such as a motor vehicle the cash debit asset converts to a vehicle debit asset.

Goods bought against sales orders are debited to cost of sales. The credit goes to reducing the bank balance.

As our goods are marked up 100%, the initial purchase of $ 20 000 goods for resale are immediately sold for cash for $ 40 000. The $ 40 000 is debited to the bank account and the bank account balance is increased by this amount. The credit goes to the sales account. The sales account records the sales as they occur and this gives a running balance. The sales account and bank account balances are usually the most important balances to keep track. As these give a good idea of your profit position and the other your solvency position.

Goods bought on credit the payment is only made 30 or 60 days from the end of the month in which they are bought. In this instance we debit $40 000 to cost of sales and $40 000 to the creditor Mr X.

Credits can go to sales, to creditors or to the reduction of the bank balance or some other asset.

Second cash sale for the month.

Payment of delivery costs reduces bank account balance

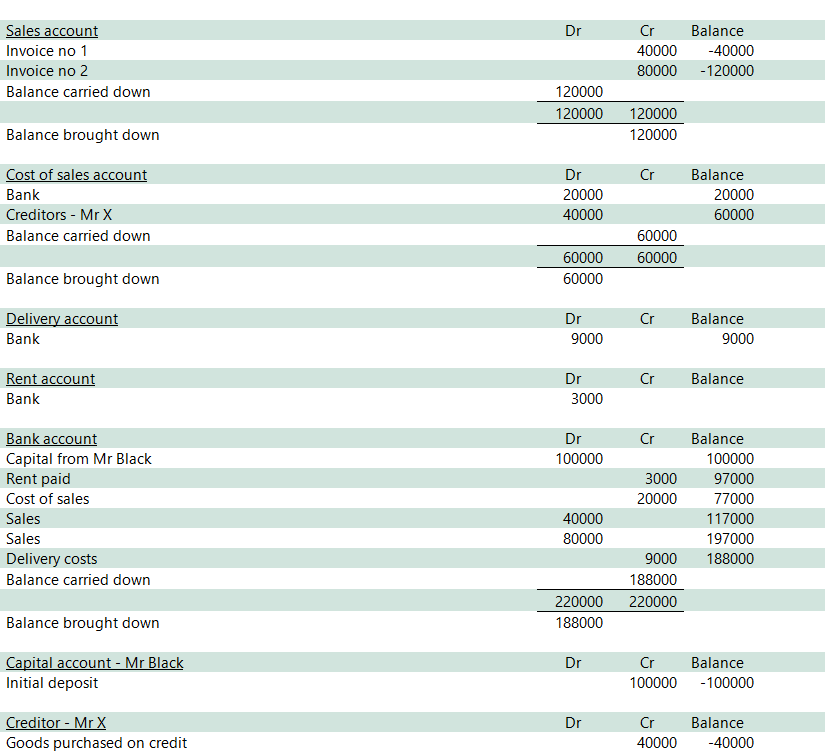

General Ledger

The entries are first recorded entry by entry in the journal book. After that they are posted to the general ledger so that running totals can be extracted as and when required.

General Ledger of Mr Pink

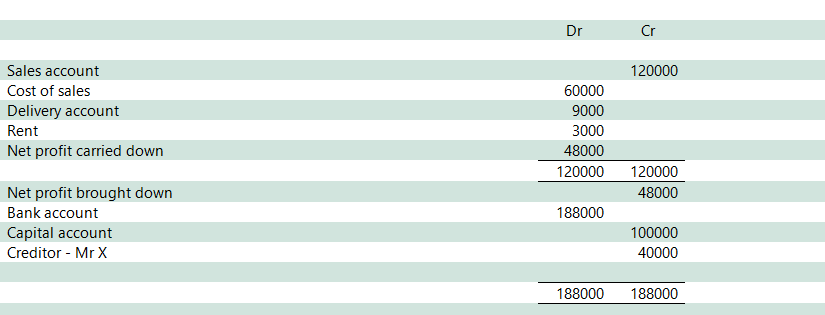

Trial balance

To ensure that all the entries have been posted it is customary to extract a trial balance. The trial balance is usually split into two sections. The income and expenses in the top section and the assets and liabilities in the bottom section.

The difference between the income and expense accounts is your net profit for the period. This amount is carried down to the assets and liability section below.

The above is a manual system which is quite time consuming. When using a computer system most time is spent entering the figures into the system. The printing of the trial balance is almost instantaneous. Computerised sales invoices are used to update the sales account as the invoices are printed. In some cases the computer systems update the stock records simultaneously.

A computer system usually reflects debits as positive numbers and credits as minus numbers. The total of the debits and credits in a computerised general ledger system should always be nil. The debits will have no sign number whilst the credits will have a minus sign in front of the number.

Trading companies usually set their accounting systems up to reflect the gross profit. This is the difference between the sales accounts and the direct cost of the goods being sold. The reason for this is to ensure that the gross profit percentage is very close to the markups. This is a very important control tool to ensure goods are correctly priced and goods are not being pilfered.

The best way of remembering which entries are expenses and revenue is to prepare a chart of accounts.

The expense and revenue categories will appear in the top half of the chart. The assets and liabilities will appear in the second half of the chart. The expenses and revenue accounts appear in the top half and the carry down amount is determined and carried down to the second half of the chart. At the end of the year this amount will represent the profit or loss for the year. This would be added to the profit brought forward from the previous years, or if a loss to be deducted from the profit brought forward.

Today when purchasing goods one uses a debit card or makes an electronic transfer. These methods move money from your bank account to the bank account of the vendor. Or by making direct transfers into the account of the vendor using the transfer form at the bank and handing this to the teller to record the transaction.

When selling goods the purchaser may pay you by debit card or deposit cash into your bank account or an EFT. Electronic transfers are made by using an electronic program whereby one enters the bank details of the seller and presses a button and the money is automatically transferred from your bank account to the bank account of the seller. The program is linked to your bank account. The transfer is effected by entering the bank details of the person or entity to whom you are making the payment. The debit card payment is made by entering your bank account into a card reading machine in the possession the vendor and the amount to be paid and sliding your debit card through that machine to authorize the payment.

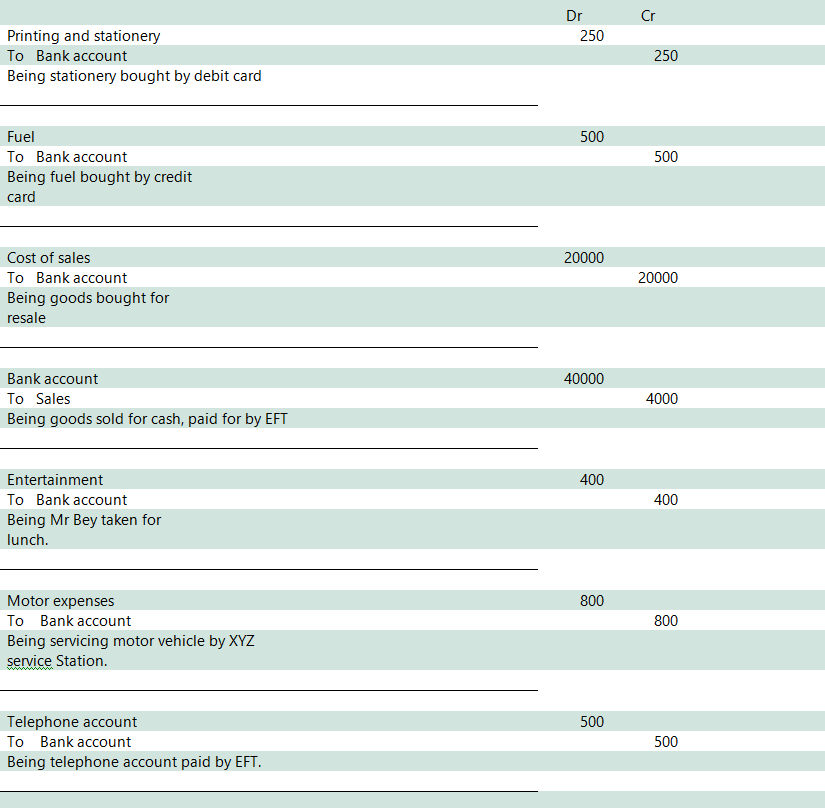

Example 2

We will now carry out an exercise to test our understanding of the journal entry to be applied to the transactions listed below: –

Stationery bought via debit card for $ 250-00

Petrol bought by credit card for $ 500-00

Goods bought for resale in amount $ 20 000 from MR Zed using the electronic payment system.

This is known as an EFT payment system.

The $ 20 000 goods bought above were sold to Mr Bey for $ 40 000. He made an immediate electronic payment into our bank account for this amount

We entertained Mr Bey at a local restaurant and paid for this using the debit card. The bill amounted to $ 400-00

The business owned motor vehicle was serviced at a local service station. The payment was made to XYZ Service Station in amount $ 800-00 by debit card.

The monthly telephone account was received from Telcom Africa. This was immediately paid by electronic transfer in amount $ 500-00

Answer to above tutorial

The rule to remember is that when payments are made the bank balance is reduced and one needs to credit the bank account. When money is received either in cash or by EFT transfer or direct deposit one debits the bank account.

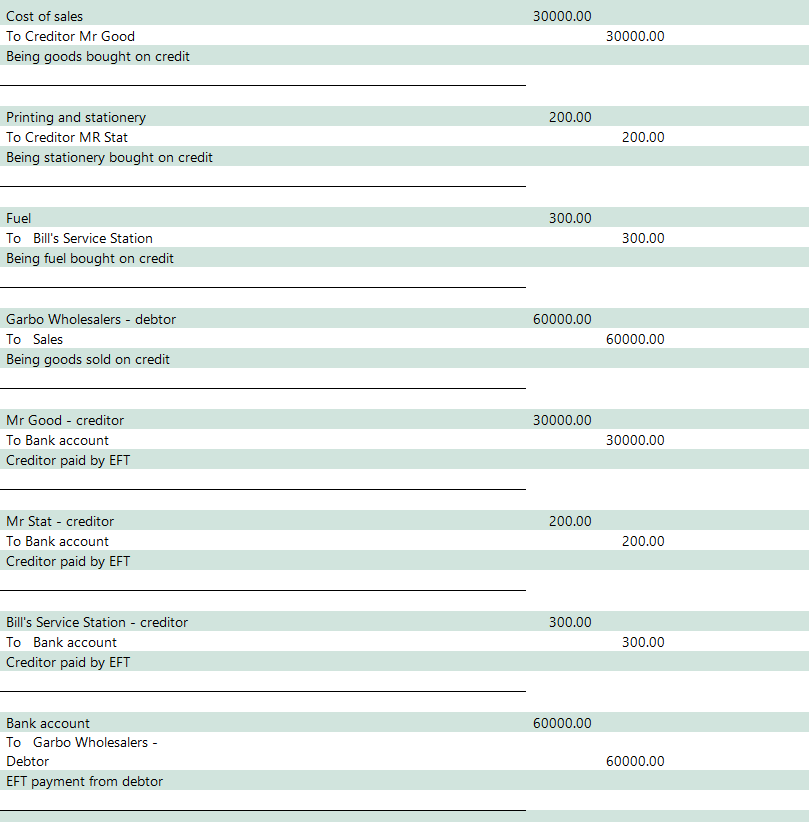

In the next exercise we will insert the creditor between the expense account and the payment. When we buy on credit then we first credit the creditor with the amount to be paid. Then when we make the payment, we credit the bank account and debit the creditor.

As the business entity grows it becomes more efficient to buy supplies from dedicated suppliers of goods and services. Usually on an ongoing basis during the month and then pay for them 30 to 60 days after the end of the month. This eliminates the necessity to visit malls and local shops to buy goods using debit cards and cash.

The situation arises with the sales of your goods. Unless you are supplying very unique goods the purchasers will only buy on credit terms to avoid having to make individual payments during the course of the month. Also to obtain the best credit terms from their suppliers.

We will now prepare the journal entries relating to the transactions listed below: –

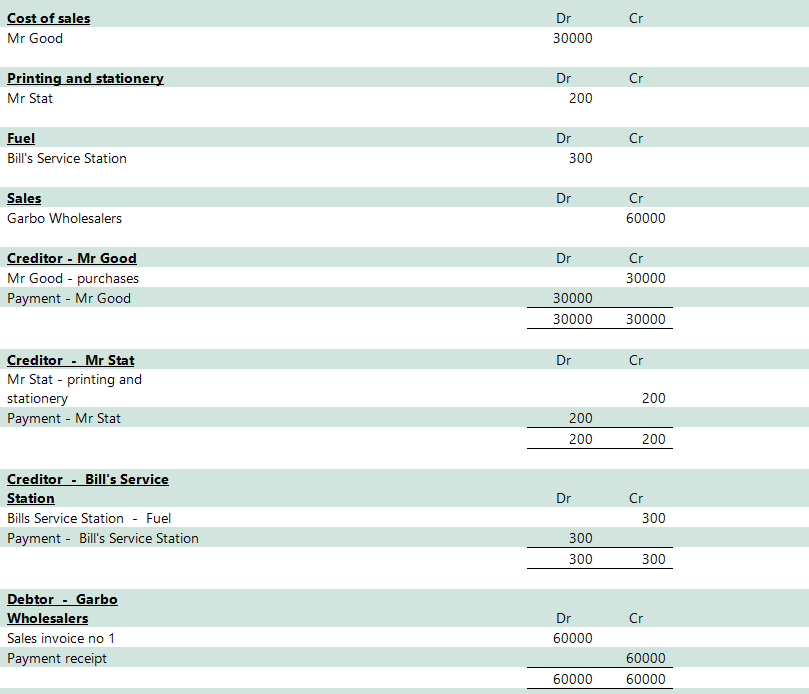

Goods for resale bought on credit from Mr Good in amount $ 30 000-00

Stationery bought on credit from Mr Stat in amount $ 200-00

Petrol bought on credit from Bill’s Service Station in amount $ 300-00.

Goods sold on credit and delivered to Garbo Wholesalers in amount $ 60 000

After thirty days we make the following separate EFT payments: –

Mr Good paid by EFT in amount $ 30 000-00

Mr Stat paid by EFT in amount $ 200-00

Bill’s Service Station paid in amount $ 300-00

On the same day Garbo Wholesalers paid us $ 60 000-00

The journal entries required to record these transactions are as below : –

The general ledger accounts will be as follows assuming that the only brought forward balances are $ 40 000 in the bank and the credit of $ 40 000 to the owner’s loan account: –

The profit excluding other overheads such as telephones and travelling and rent amount to $ 29 500 and the trial balance is in balance which means all entries have been accounted for, plus the cash book balance agrees with the bank statements balance so all payments have been brought to account.

The trial balance above was extracted before the end of the month and in all likelihood there would be bank charges plus debits for monthly stop orders such as internet usage, and salary payments or personal drawings by the owner.

The “Early Cash Book”

The cash book as taught in the school system in the late 1950’s I have called the “Early Cash Book” and a specimen of that cash is available for your perusal. The world population at that time was a lot less and the banking system was a lot slower with smaller volumes of transactions.

Payments were made by way of cheques and post-dated bills and cheques were manually delivered to the bank. Cheques were drawn at the end of the day on which they were cashed or deposited. In the case of cheques drawn on towns and cities in another province or county or state this often took quite a few days.

The early cash book reflects a bank column and a cash column, often the cash was used for sundry purchases and the balance deposited into the bank and a contra entry was made showing the deposit in the bank column on the debit side of the cash book and the cash payment entry on the credit side of the cash book in the cash column.

The business practice at that time was to have a separate petty cash book for cash purchases and a separate cash book. Usually there were two cash books, one for payments and one in which the actual bank deposits were entered. The school version resulted in wasted paper as many pages would be lost arriving at the final cash book balance on the same page of a double page cash book.

Benefits of EFT

It is only with the advent of the EFT system that the cash book and bank statements can be agreed without any differences due to cheques not yet being cashed by the payee for a number of days after being drawn due to delivery delays, especially in countries with bad postal systems.

In a simple manual set of books one would incorporate the cash book into the general ledger thereby not having to pass journal entries into the accounting system in respect of cash book entries. This is accomplished by cross posting from the cash book. The deposit for instance would be entered on the debit side of the cash book. The credit entry would be recorded in the account relative to the nature of the deposit. If it was interest received. Then the credit would be entered on the credit side of the interest received account, if it was cash sales the credit would be entered on the credit side of the cash sales account.

Folios

Custom produced cash books, journals and general ledgers are printed with consecutive page numbers making it easier to cross reference the entry. The pages are referred to as folios. When you see the word folio in the heading it signifies that the responding entry has been posted to that folio. We enter a J in front of the number if it is a journal entry, a CB, if it is a cash book reference and a GL for a general ledger reference.

The simple double sided cash book is rarely used in practice as the detail column and folio column can be used on the same page with two columns for debits and credits. That or plus or minus signs in the one column depicting debits and credits. The most common system is two cash books one for receipts and one for payments. The reason for this being that the receipts cash book usually contains direct deposits and part payments and EFT payments and unless large expensive items are sold there are many more receipts from debtors.

We will deal with the books of prime entry. These are designed to reduce the number of posting items by consolidating various entries into one posting column. The books of prime entry consist mainly of separate books for the cash book, sales journal, purchase journal, petty cash book and possibly a bill payable and bill receivable book.

Depreciation of fixed assets

Another journal entry is the depreciation of certain fixed assets which have a limited useful life. These assets are written down by raising a depreciation charge against the asset each year. The usual asset class being furniture and fittings, office equipment, computers and motor vehicles. Furniture and fittings usually depreciate by 10% – 15% per annum until they reach what is considered their fair value. Then they are reflected by an amount of the fair value in the following year. Computers are usually depreciated by 33 % per annum as they usually become obsolete within three years due to advancements. Office equipment is usually depreciated by 20 % per annum. Motor vehicles are usually depreciated by 20 % per annum.

Land and buildings might appreciate over a reasonable period. It is prudent to revalue the land and buildings to market value every three years.

When determining the annual charge the number of months in use in the year are calculated and the charge is pro-rated on a time basis. A vehicle bought on the first day of the financial year, costing 100 000 dollars. Would depreciate by 20 000 dollars for the year and the entry would be as below: –

The depreciation charge of 20 000 dollars is debited to the expense section of the general ledger as this is an expense. Reducing the original cost of the motor vehicle. The credit goes to the “provision for depreciation – motor vehicle account” in the asset and liability section of the general ledger. A separate provision for depreciation account is used instead of crediting the cost of the motor vehicle account. In the case of a limited company the original cost of the fixed assets must be shown separately from the depreciation charged to date.

Provision for expenditure

The provision for expenditure applies to a task which is charged to the expense section of the general ledger but which is incomplete at the year end date. The provider will only raise an invoice after the year end. It is then incumbent in the case of a limited company to estimate the proportion of the final cost incurred to the year end date. In this case the final cost is sixty thousand dollars, and it is fifty percent complete

at the year end date, then the provision required is fifty percent. For the purposes of our example the task is the audit of the company for the current year. We make a provision for audit fees of thirty thousand dollars for the year. This is an expense so the debit goes to the expense portion of the trial balance. The credit to the liability section of the general ledger and the entry is as follows: –

When making payment one would split the payment debiting thirty thousand dollars to the “Audit fees account”, and thirty thousand dollars to the “Provision for expenses account”. This payment is made in the following year.