Books of Prime Entry

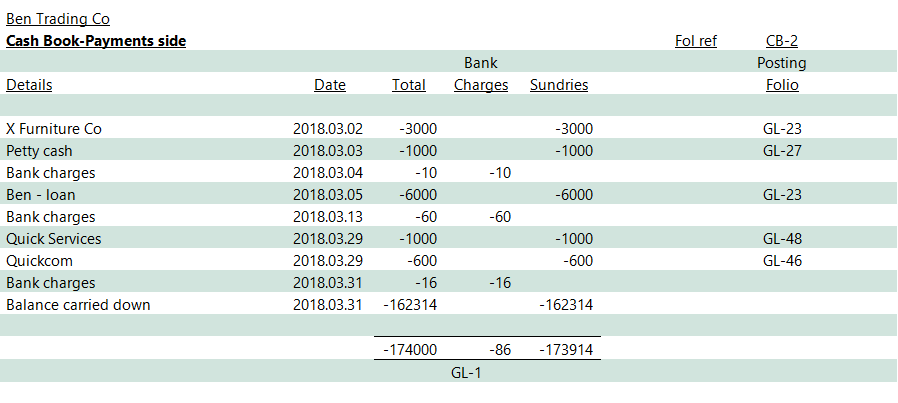

Books of prime entry are used to summarise entries. Entries which relate to the same ledger accounts to avoid making repetitive journal entries. The main books of prime entry being the sales journal, purchases journal, cash book and petty cash book.

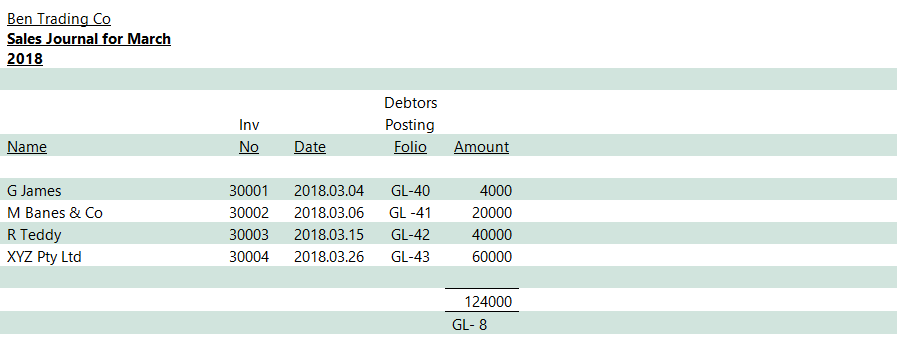

We will deal with these one at a time beginning with the sales journal.

The information we need to record in the sales journal includes

the name of the purchaser,

the invoice number,

the date of the transaction,

the gross amount of the goods sold

and the posting folio of the debtor to keep track of amounts outstanding.

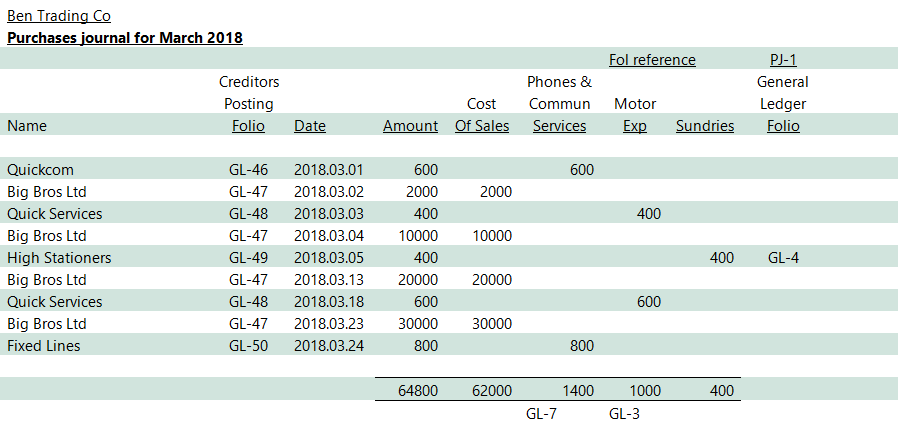

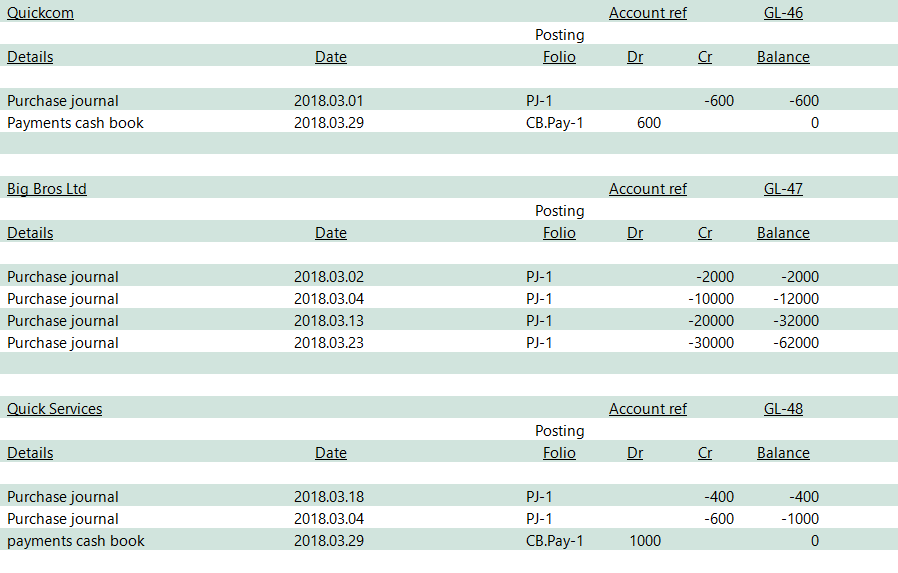

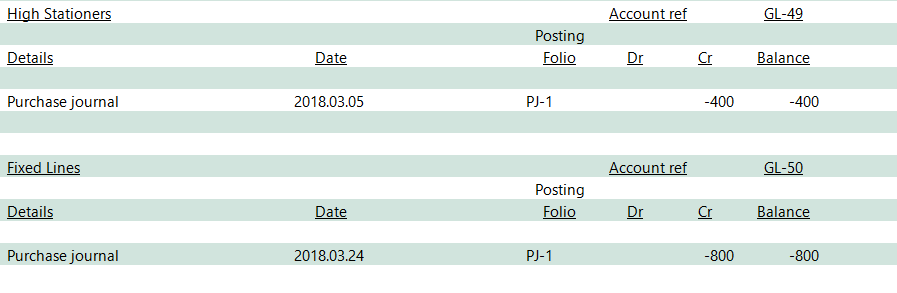

We will now prepare the purchase journal which is used to record goods and services bought on credit. We will need to record the name of the supplier, the posting folio, the date of the transaction, the amount of the transaction split into cost of goods and services and the expense account either at the bottom of the expense column or in the right-hand column if it is a seldom used purchase.

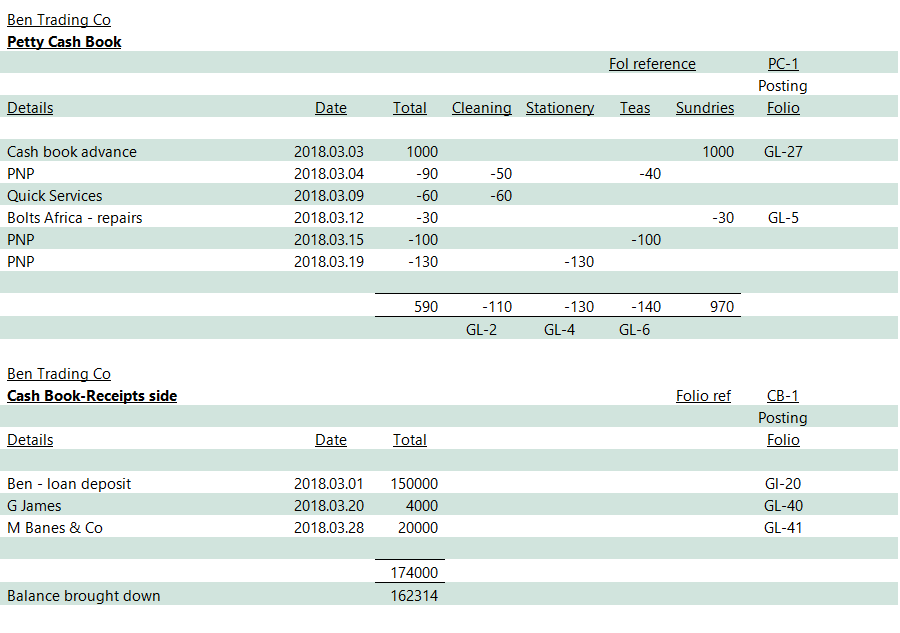

The petty cash book is used when goods and services are bought on COD. Also when employees who are not permitted to use credit cards need to purchase items on behalf of the business are reimbursed.

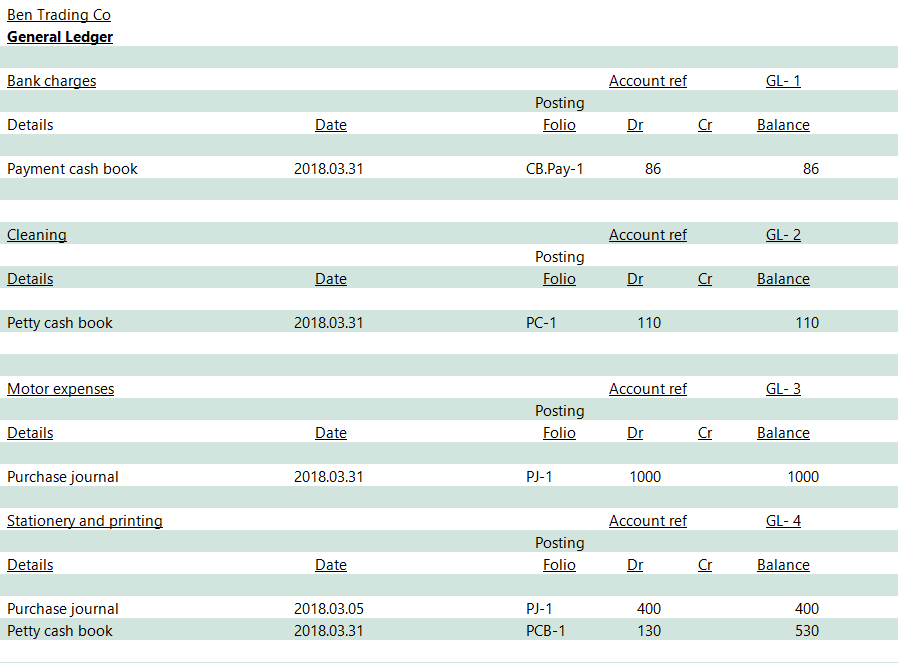

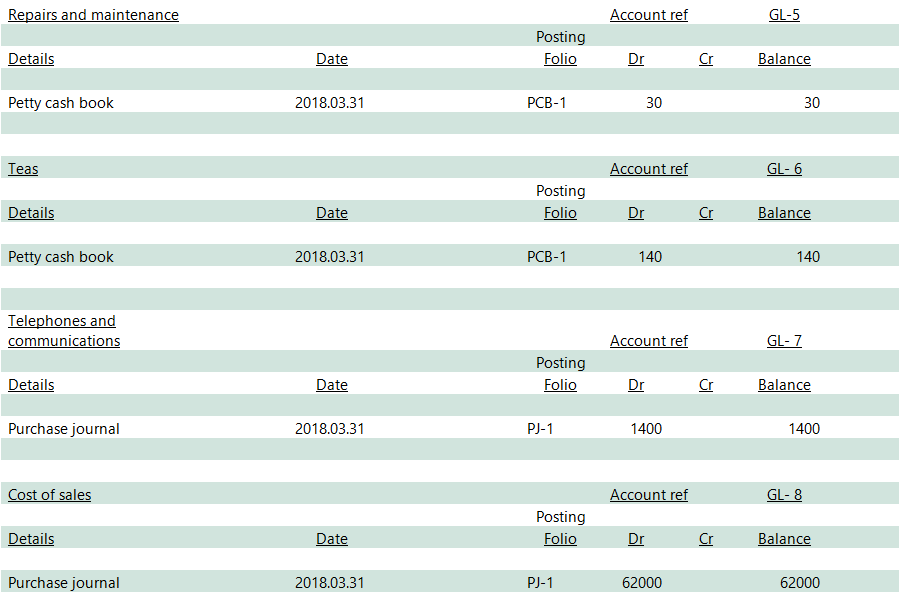

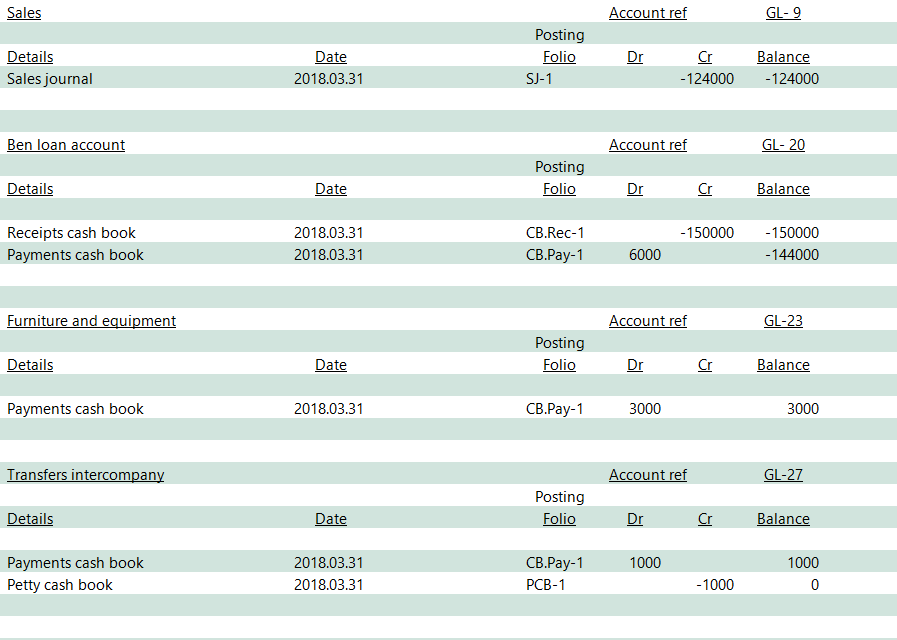

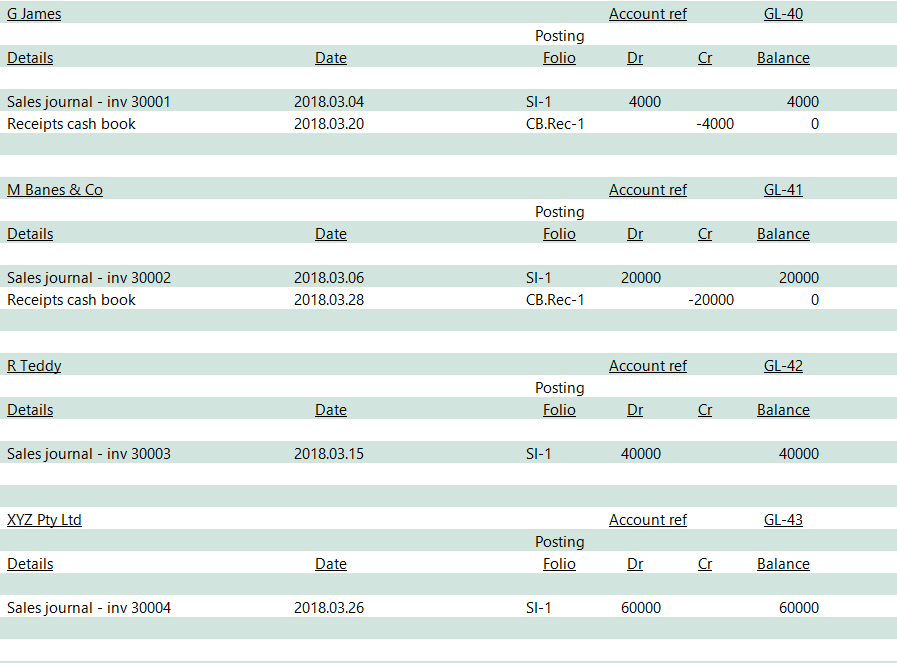

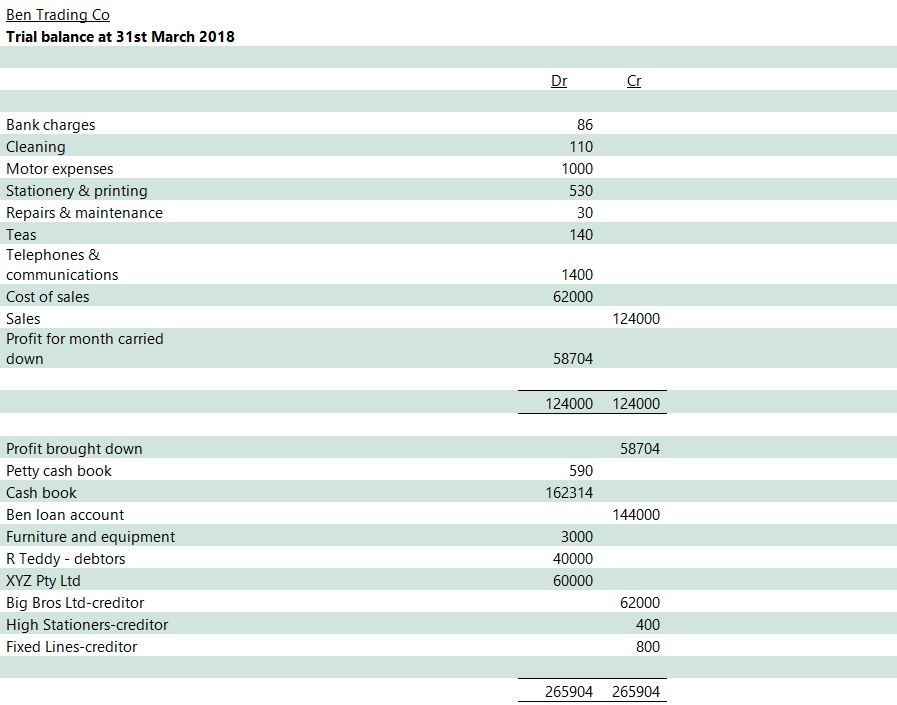

The below trial balance was extracted from the general ledger to prove the accuracy and completeness of the general ledger

Points of interest

If you total the assets and liabilities the assets will exceed the liabilities by R 58 704.

It is more presentable to list the income and expenses first.

The profit then shows as a credit emphasising that a profit was made.

Since this was the first month of trading no balances forward are reflected from prior periods.

The petty cash book is treated as part of the general in the same way as the cash book so the closing balance is included in the trial balance as is the cash book balance.

When preparing the ledger accounts, we used minus signs to depict credit balances and the same was applied to the cash book and petty cash book. Minus signs represent a reduction of the bank balance and the cash on hand reflected in the petty cash book.

The “Transfers inter-company” account is used to ensure that payments between the cash book and the petty cash book are cancelled out. In larger companies situated in different towns and cities there might be more than one bank account. This account is used to ensure that any payments between the branches are brought to account.

When using a manual ledger the number of lines between each account would vary quite considerably as the remaining lines per page would depend on the number of entries in each page. In the above example it would be idiotic to leave numerous blank lines between each account. A computer ledger system is programmed to leave two lines between each ledger account to save paper.

I suggest if you have no experience in posting up a general ledger that you “screen save” copies of the books of prime entry. Creating the general ledger from scratch and perform the postings to that ledger. Confidence comes from actually performing the task.