Trust bank accounts

Certain industries require the owner of the business to open trust bank accounts into which monies belonging to their clients are deposited. Lawyers, solicitors, estate agents and stockbrokers immediately come to mind.

Lawyers

Solicitors and lawyers accept advance payments for services to be performed. Also amounts to be paid to third parties in the performance of their duties. These duties include the purchase and sale of fixed property, shares and many other asset classes. The legal profession requires them to only draw down client deposits once they have performed the relevant task. Also only on the issue of an appropriate invoice.

Estate agents

Estate agents are similarly required to deposit client monies into a trust fund or place the money with a lawyer or solicitor pending transfer of title of the property they have undertaken to sell or purchase on behalf of the client.

Stockbrokers

Stockbrokers are required to separate their clients’ funds from their own funds. Stock exchange systems are very sophisticated and they may provide for the client transactions to be performed inhouse. When this is the case they usually provide for the client’s cash balance to be swept into a trust bank account at the end of each day. This is accomplished by totalling the balance to the credit of each client in respect of each broker, and transferring that amount to the trust account. The money is returned the following day. This permits the stock exchange to monitor the solvency of each stockbroker and ensure that they meet the capital requirements to continue in business.

Certain trading platforms are operated outside the control of the stock exchange. Although the transactions are effected through the stock exchange trading computer system, they are required to provide security and guarantees to cover gross amount owing to the stock exchange at the end of each day.

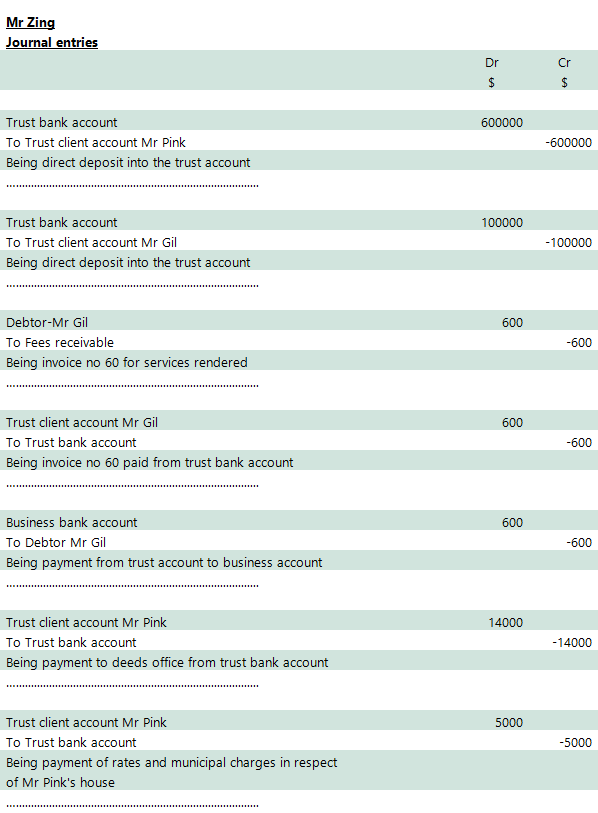

Example no 1

A solicitor during the course of a week’s business activities records the transactions listed below in the conduct of his business. The solicitor Mr Zing is a sole trader and employs two other persons. Record the transactions below via journal entries: –

1. An amount of $ 600 000 is transferred into his trust bank account by Mr Pink to cover the cost of purchasing a house for $ 570 000. The amount in excess of the purchase price is to discharge any fees and costs involved in the transaction.

2. Mr Gil consults with Mr Zing in connection with impending legal action regarding his dog attacking a passerby. He transfers $ 100 000 dollars into his trust account to cover legal costs. Also providing for settlement of the looming claim for damages.

3. Mr Zing raises invoice no 60 for $ 600 to cover his time spent researching similar cases and the time spent in his initial consultation with Mr Gil

4. Mr Zing transfers $ 600 from the trust account to his business account to cover invoice no 60

5. Mr Zing makes a payment of $ 14 000 to the deeds office to cover transfer duties in respect of the purchase of Mr Pink’s house. This is paid from the trust account

6. Mr Zing makes a payment to the local authority in respect of outstanding rates and municipal charges relating to Mr Pinks new house in amount $ 5 000. This payment is made from the trust account.

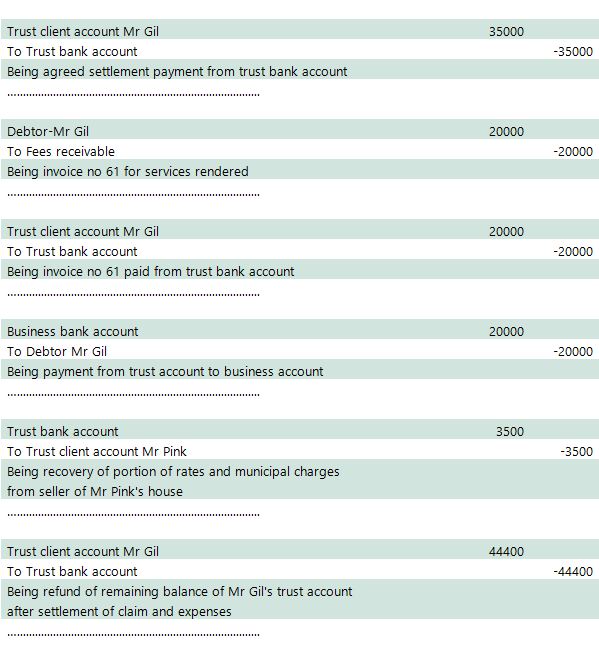

7. Mr Zing reaches an out of court settlement with the solicitor of the party injured in the incident concerning Mr Gil’s dog. He makes an eft payment to Solman & Co being the solicitor of the claimant in amount $ 35 000 in full and final settlement.

This payment is made from the trust account.

8. Mr Zing raises invoice no 61 for $ 20 000. For services in dealing with the the claim against Mr Gil.

9. Mr Zing transfers $ 20 000 from the trust account to his business account to cover invoice no 61.

10. Mr Zing recovers $ 3 500 from the seller of Mr Pink’s house in respect of the seller’s portion of the rates and municipal charges

11. Mr Zing makes an eft refund from his trust account to Mr Gil in amount $ 44 400 being the remaining balance after conclusion of the damages claim.

Note

The payment from the trust account to the business account requires two separate journal entries. This is because the equal and opposite entry has to be generated from two different bank accounts. In practice the entries would be passed as the book-keeper processed the bank account statements. It is unlikely that these would be successive entries as recorded above. As the book-keeper would complete the one bank statement before attending to the bank statement of the second bank account.

It is essential that the bank balance is equal to, or exceeds the total of the total of the client trust accounts. Advances to one trust creditor may not be financed out of the credit balances of another trust account creditor.

The bank charges relating to the trust bank account are usually debited in the business bank account as this is a business expense.

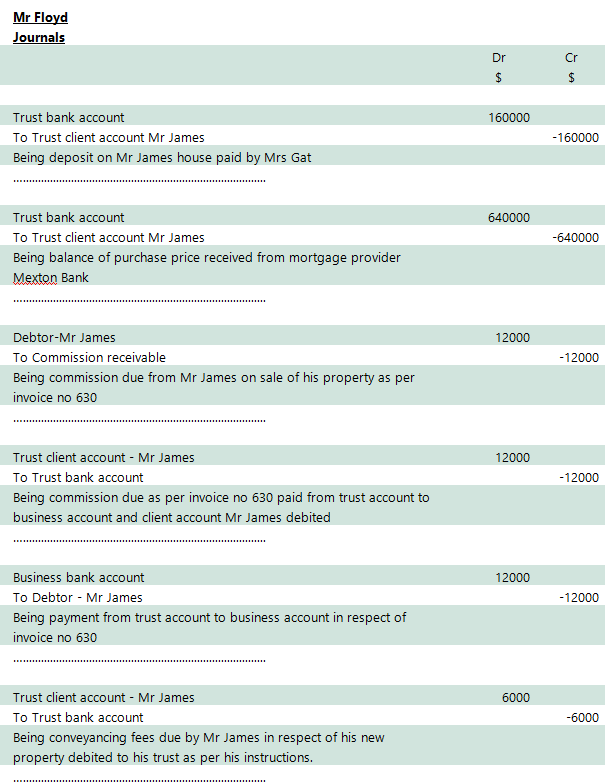

Example no 2

Estate agents are also required to deposit client monies into a trust bank account and may only claim their commission on the final completion of the transaction.

The usual practice is for the seller to pay the commission selling agent and the purchaser to pay the deeds transfer costs to the transfer conveyancer.

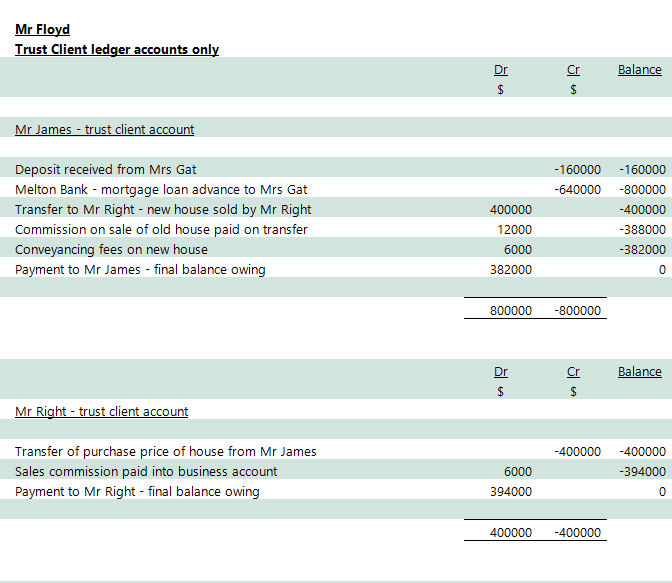

Estate agent Floyd conducts his business as a sole trader and employs two sales staff on a commission basis. Record the transactions below via journal entries, in addition the entries in each individual client trust account: –

1. Mr James accepts a sale contract to sell his house for a gross sales price of $ 800 000 and he agrees to a commission rate of one and a half percent on the gross selling price.

2. Since it is his intention to downsize Mr James makes an offer on a smaller property in amount $ 400 000 which is duly accepted. The seller is Mr Right, and he agrees to a commission rate of one and a half percent. Both purchaser and seller agree to Mr Floyd handling the transaction. The second transaction is conditional on the sale of Mr James larger house and no deposit is payable, but the full purchase price is payable on transfer of the property.

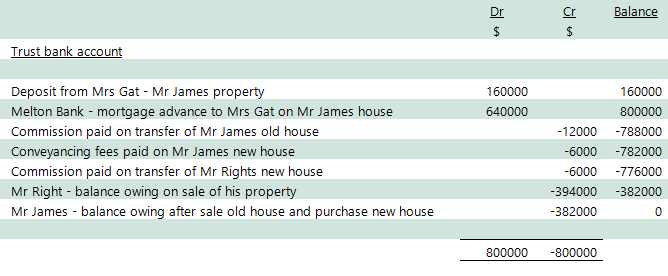

3. The purchaser of Mr James house pays a deposit of $ 160 000 which is deposited into the trust account. Mr Floyd instructs the conveyancer to prepare the transfer documents to enable a simultaneous transfer of the two properties. Prospective purchaser being Mrs Gat

4. On the transfer date the mortgage provider pays the balance of the purchase price to Mr Floyd. This amount of $ 640 000 which is credited to the trust client account of Mr James via the trust bank account.

5. Mr Floyd raises invoice no 630 in amount $ 12 000 in respect of the property sold by Mr James.

6. Mr Floyd transfers $ 12 000 from the client trust account to the business account. This covers the amount due in respect of invoice no 630.

7. Mr Floyd also makes an eft payment to the conveyancer of $ 6 000. This is the balance due by Mr James in respect of the transfer fees in respect of his new property

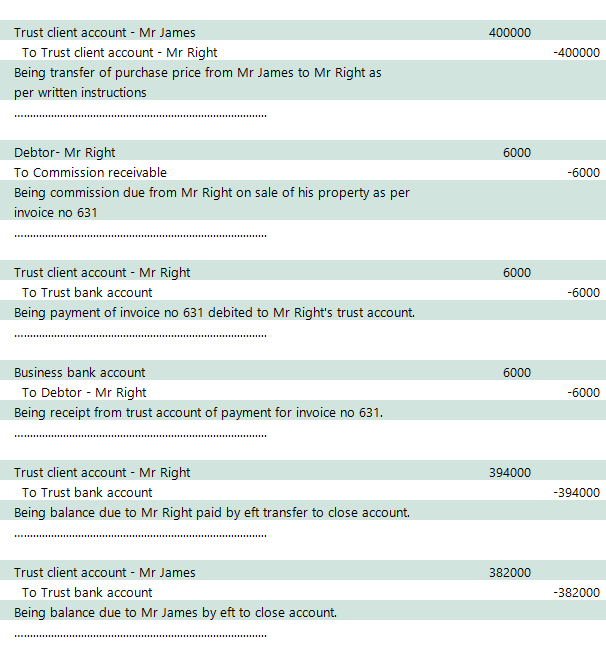

8. Mr Floyd passes a journal entry transferring $ 400 000 dollars from the trust account Mr James to the trust account of Mr Right. This is the full purchase price on the property bought by Mr James.

9. Mr Floyd raises invoice no 631 in amount $ 6 000 being his commission due by Mr Right on the sale of his house. This is debited to Mr Right’s account in the business account

10. Mr Floyd transferred $ 6 000 from the trust bank account to the business account in payment of invoice no 631 and this was debited to Mr Right’s client account.

11. Mr Floyd paid the balance due to Mr Right by eft in amount $ 394 000.

12. Mr Floyd paid the balance due to Mr James by eft in amount $ 382 000.

Note

There were not many transactions but to record them accurately requires attention to detail. A quick glance at the question and one would think this is a very simple question. However, the transfers between the bank accounts requires one to account for the entries on the bank statements.

The fact that the client trust accounts are reduced to nil plus the trust bank account balance gives one confidence that all entries have been brought to account.

In examination conditions one would probably not use credit signs on the credit entries and balance column could be ignored.

Pension funds

The pension fund is a trust entity governed by statutes. The rules are drawn up to control the administration of the specific pension fund. The statutes usually require that a certain percentage of the pension funds be invested in secure government investments.

Pension funds governed by quoted companies have been raided by certain quoted companies over the years. The rules sometimes provide for the companies to make up any shortfall in the fund. When there are surpluses certain quoted companies have helped themselves to the surplus. In certain instances, they have acquired other quoted entities with the sole purpose of accessing the pension fund surpluses.

Inflation has caused certain pension funds to become vulnerable. Sometimes pension funds controlled by the management of the employee company might fail to pay the contributions to the pension funds.

Another unfortunate outcome is that government and SOE controlled entities are badly managed. Political parties may appoint unfit managers, and officials who are employed at excessive salaries and then entitled to very high pension settlements.

Pension funds are usually subject to audit. Sadly by the time the audit is completed the damage has been done. Also, it is very difficult to try and recover excessive payments to political appointed officials as the political party usually controls the judicial system.