Computerised accounting systems

In most small businesses a standard computer package is adequate in providing for the requirements of the business. There are usually modules that can be incorporated into the standard general ledger package according to the needs of the client. If multiple small credit sales are made then one would incorporate the debtors ledger. If the same applied to purchases then one would incorporate the creditors ledger and possibly a stock ledger.

The general ledger accounts each have a separate numeric number, and this is displayed in a chart of accounts. Usually, one can add a general ledger account and allocate a new reference number to that ledger account. The ledger account numbers are usually spaced and the expense accounts are in alphabetical order so one can slot an account into the chart of accounts and still maintain the alphabetic and numeric order. One can also create one’s own chart of accounts.

The Ledger

The ledger is also designed so that certain sub accounts are added together to give one total when requested. One may split the petrol accounts for each employee but only request the sub accounts on certain occasions. Usually being satisfied with the total of the employee petrol accounts. The same could apply to say the telephone and internet accounts where the total amount is usually sufficient. The total being requested here being the trial balance total. When viewing the general ledger, one would see all the sub accounts

The debtors and creditors ledgers work on the same principle with only the total of these accounts being included in the trial balance aptly referred to as control accounts. This would apply where each entry is activated separately on a real time basis and every entry appears separately in the general ledger. Where the general ledger is updated using batch listings then each item in the batch is inputted into the debtors or creditors ledger from the pre-printed list and the total of each batch inputted into the respective control ledger account.

When creating the batch listings, the individual items would be coded separately, but only total of the batch listing would be coded and posted into the general ledger control account.

Important to Note

The use of batch total postings requires very careful attention to detail with the listings being meticulously filed. To ensure all entries on the listings can be reconciled back to the deposits in the bank account and all sales invoices accounted for with respect to invoice sequence numbers.

Most standard general ledger packages also generate listings of batch postings and these need to be printed and filed for verification purposes. The totals of the debtors listing and creditors listing agreeing with the amounts appearing in the respective control accounts.

Computer packages are designed to have separate input sub programs for the cash book, sales, purchases and journal entries. Then there is the display section where one views the general ledger, extracts trial balances and sometimes produces financial statements for management purposes.

Operating Manuals

Standard computer packages usually provide operating manuals.

These enable the user to understand and activate the various sub programs and produce reports. Programs that are specifically written for a business often lack detailed operating manuals because the programmers lose interest in the project once it becomes functional. They also fail to understand that very simple procedures in their view are not that simple to the ordinary person.

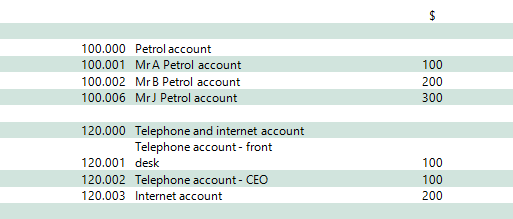

A typical coding set up with respect to expense accounts would be as follows: –

If one requested that the sub accounts be included in the general ledger trial balance printout. Then the above accounts would be separately reflected in the trial balance together with the rest of ledger accounts. If one excluded the sub accounts from the trial balance printout. Then the petrol account 100.000 would reflect a gross debit balance of 600 dollars, the telephone and internet account 120.000 would reflect a gross debit balance of 400 dollars.

The major advantage of computer systems is the speed at which information is processed. The disadvantage is that the system can become corrupted, and data lost. A big problem today is that systems are deliberately hacked. Viruses are implanted into the system to cause loss of data and impair the processing abilities of the basic program. Security measures are usually installed in major businesses to try and prevent this happening. Copies are made of the electronic ledger system at the end of each day for a predetermined number of days. This will enable the business to reprocess lost data from the point at which the problem manifested itself.