Financial statements

Limited companies are required to prepare Annual Financial statements in most advanced countries which adhere to the capitalistic system. The shareholders of Limited companies are permitted to limit their exposure to any loss to the amount of their paid-up shares provided they ensure they do not trade recklessly and do not trade whilst in an insolvent position. The shareholders of large companies rely on management to conduct the business of the company and they appoint auditors to ensure that management obey the laws of the country in which they are registered. The auditors are liable to be sued for not carrying out their duties and the directors are also liable for reckless conduct.

Individual traders and partnerships are liable to make good any loss they cause up to the extent of their net asset worth. Creditors are entitled to apply for sequestration of individual traders and members of a partnership with certain exceptions.

Limited companies are obliged to provide their shareholders with annual financial statements. A shareholder with a very small shareholding would have access to their financial results. To guard against giving away operational secrets to competitors the companies only publish dead minimum information. Standards of minimum disclosure have been formatted by accounting standard boards around the world. Investors will not invest in your company unless you comply with those standards. So the accounting authorities of most advanced countries adopt those standards to encourage business investment in their countries. The usual and most widely adopted standard appears to be full IFRS and IRFS for SMME’s.

Business Types

The type of business carried out by the company determines the way in which the company annual financial statements are drafted. In the case of ordinary trading companies buying stock for resale, one would show sales less the cost of sales giving the gross profit. The overhead and administration expenses would then be totalled and deducted from the gross profit to give the net profit. In the case of service companies and commission earning companies the gross commission would be displayed. All other expenditure would be shown in a column and deducted from the gross commission in one globular amount.

Service companies by their nature usually provide services delivered by employees and the salary bill is usually the main cost item. Construction companies usually carry out work in terms of a contract awarded to them and they receive lumpsum amounts which are known as draws or progress payments as they complete phases of the contract.

A quantity surveyor usually prepares the worksheet and estimates the value of work done and percentage of the contract price to be paid to them. Another interesting business is housing development and here one allocates the cost of the completed houses to the sales revenue received and shows the balance in the work in progress.

Notes on the below example

Since in the example below there is only one shareholder, we will not bother with minimum disclosure and only add notes where the accounts do not disclose sufficient information.

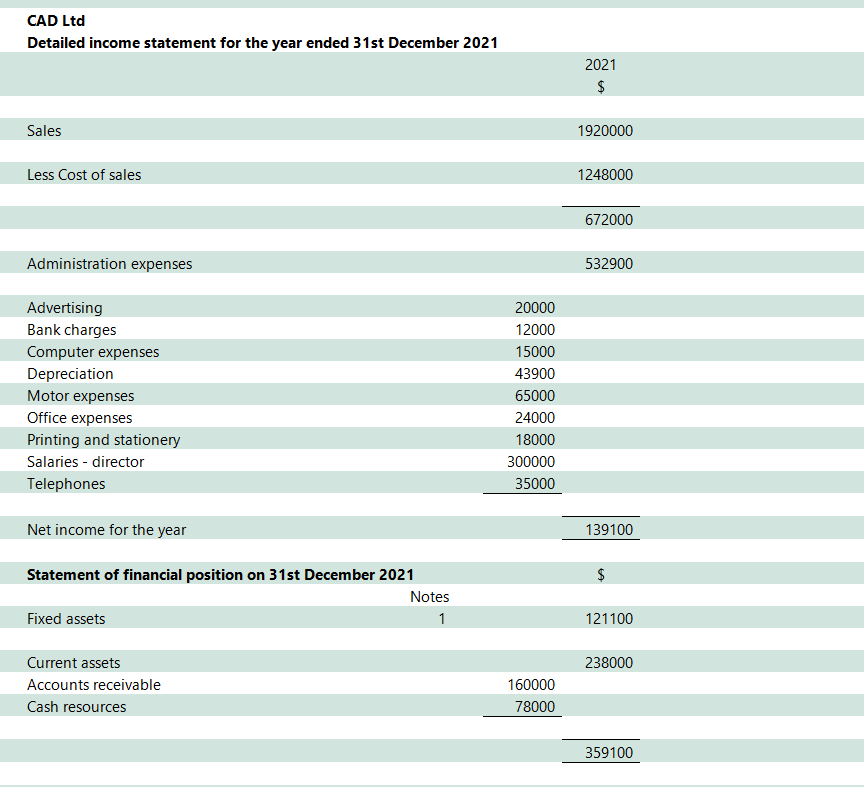

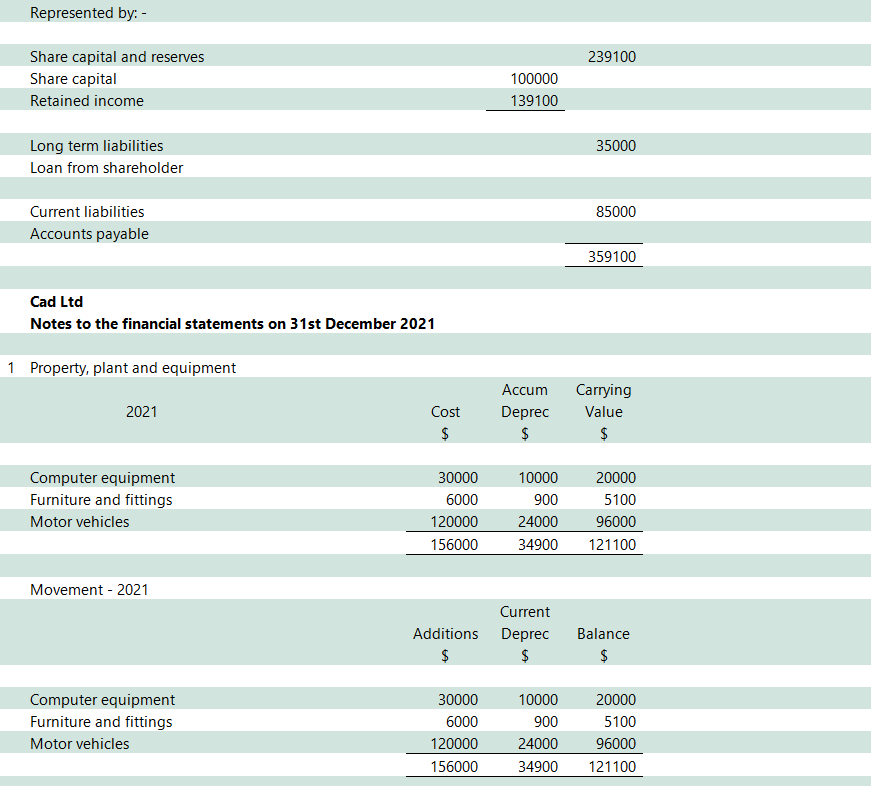

We will begin with very simple accounts and limit the notes to the fixed assets. We will then progress to more complicated accounts. There is no intention of complying with the laws of any specific country or framework as this example is a teaching exercise to give guidance as to the structure of the income statement, statement of change in equity and balance sheet.

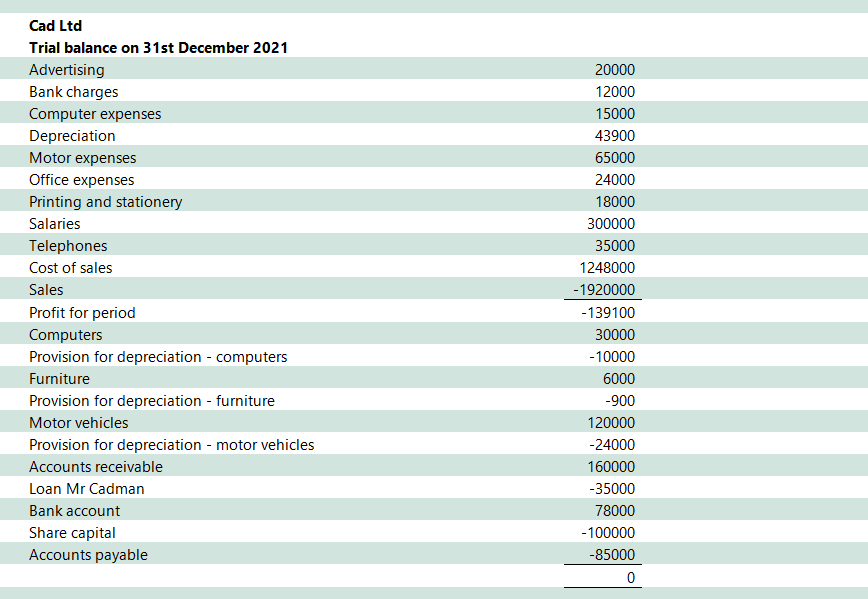

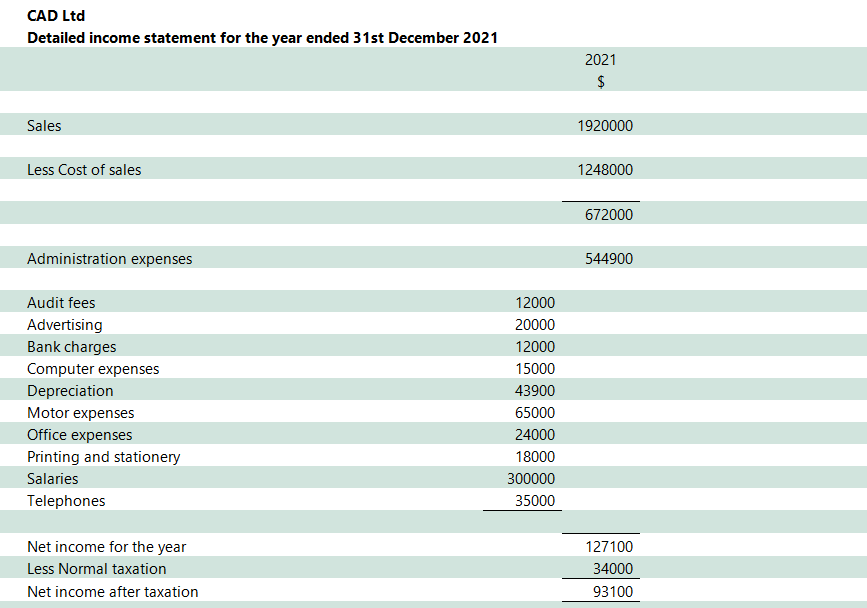

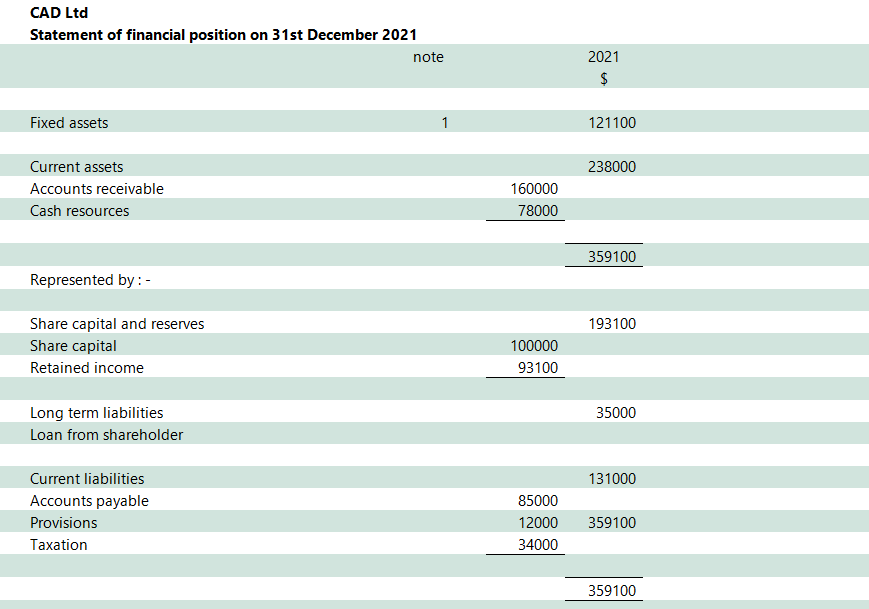

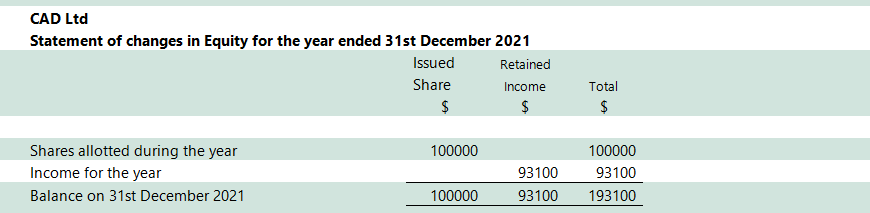

Example 1

This is the first year of trading so there are no comparatives

The computer package created the financial statements below which are for management purposes and these were delivered to the incumbent auditor for review and audit.

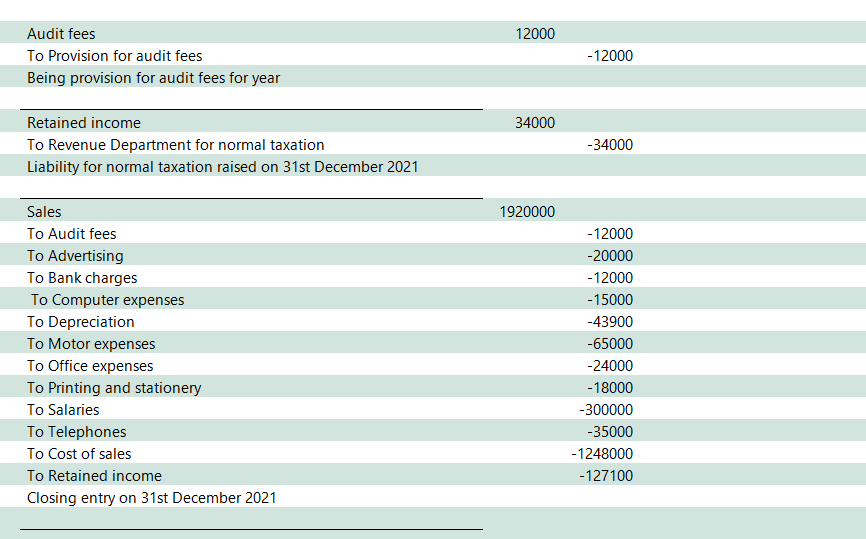

The auditors suggested certain adjusting entries with which the sole shareholder was happy to comply and the audited accounts were prepared and delivered. These entries were as below: –

The above closing journal entry is necessary for any manual accounting system since the books need to be closed off and the opening balances carried down to the new year. Some computer systems also need to be closed off if the system does not allow for automatic transfer of the expense and revenue accounts to the retained income account.

The income tax charge for the year needs to be debited straight to the retained income account. Some accounting packages reflect the income tax charge in the income and expenses portion of the trial balance which is completely misleading as income tax is not a trading expense. An additional problem is that the amount shown as being the tax charge for the year is usually wrong in that payments relating to prior years are often included in this account instead of debiting the liability account.

Comparing this balance sheet to the earlier accounts forwarded to the auditors indicates that the retained income has been reduced by forty-six thousand dollars. Provisions have increased by twelve thousand dollars and the tax liability by thirty-four thousand dollars. Together this amounts to the forty-six- thousand- dollar reduction in the retained income.

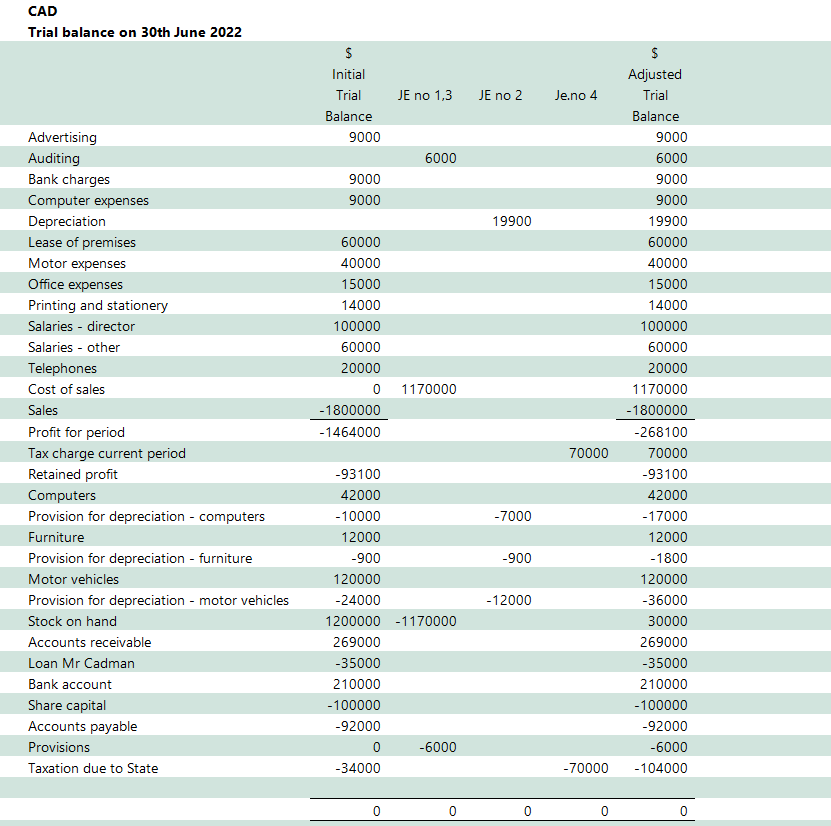

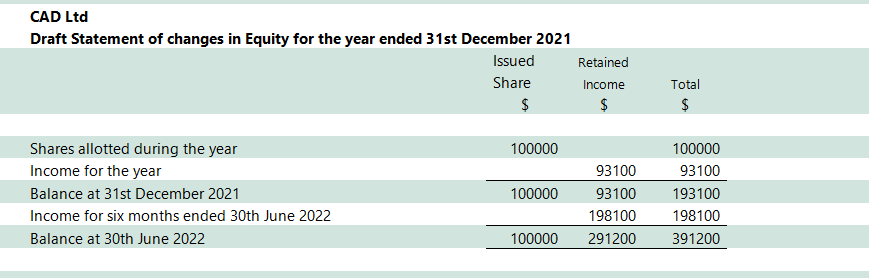

Example 2

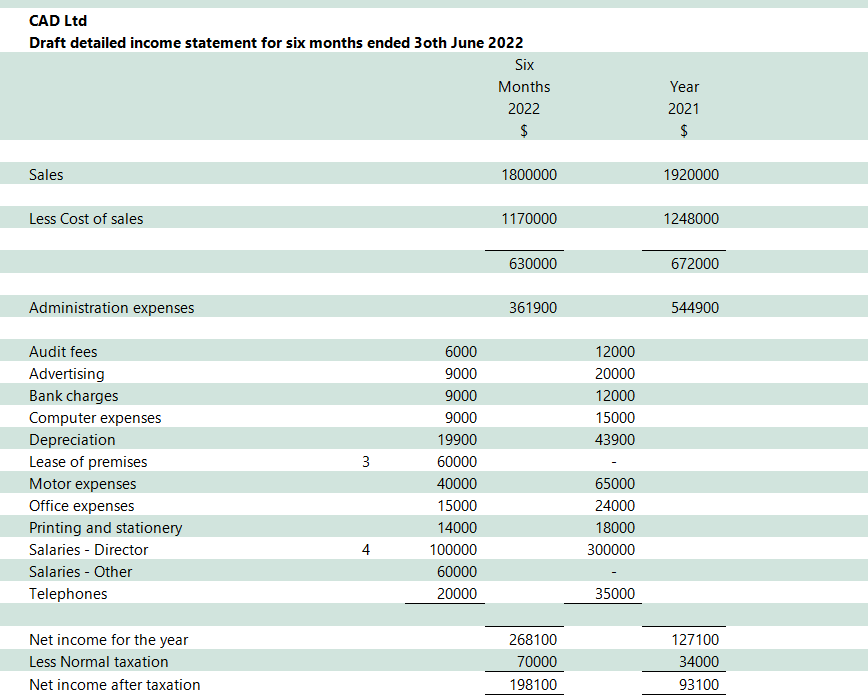

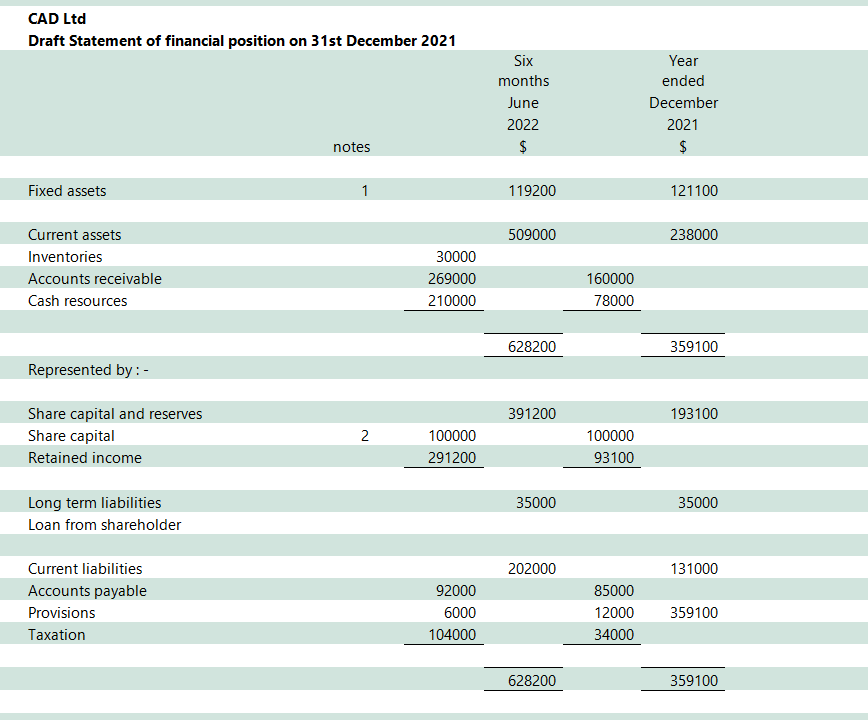

Just after six months into the following trading year CAD Ltd is offered a major contract worth five million dollars. To enable the company to finance this contract the company will need an overdraft facility of two and a half million dollars. The bank want management accounts for the six months to 30th June 2022 to make a judgement call on the risks involved in granting an overdraft of this magnitude.

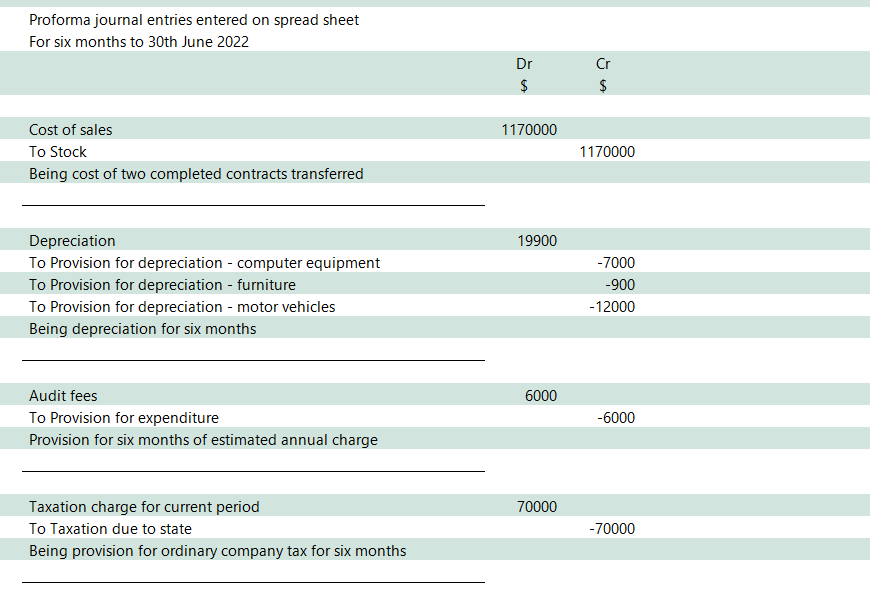

The trial balance is extracted. It is discovered that depreciation is still to be provided on the fixed assets. Also cost of sales have not yet been allocated from the stock account in respect two completed contracts. In addition, the stock on hand is still to be determined.

The director counts stock on hand which amounts to 30 000 dollars. The amount to be debited to cost of sales is one million, one hundred and seventy thousand dollars. This is in line with the previous year’s cost of sales percentages. Also in line with the costing records when quoting on the projects.

This we refer to as a running trial balance. We use the general ledger trial balance and then adjust in the journal entry adjustment columns until we are satisfied that the figures are representative of the current six months of trading. Taxation we provide for at twenty-five percent of the current taxable income.

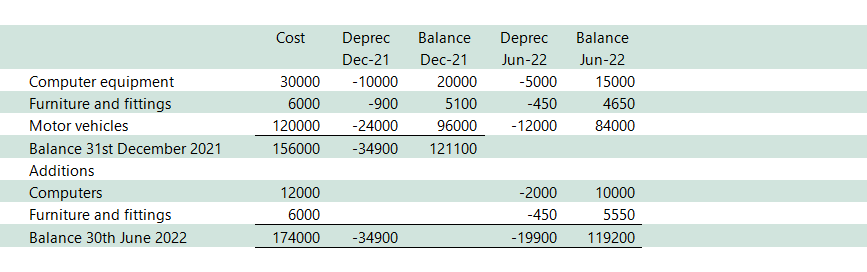

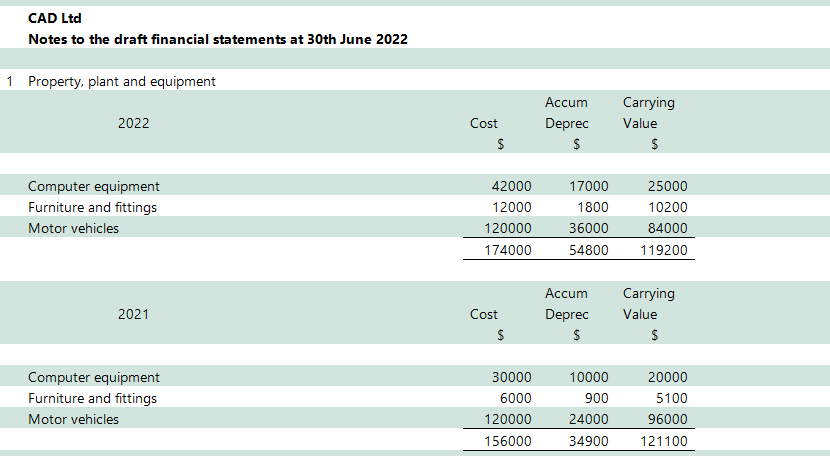

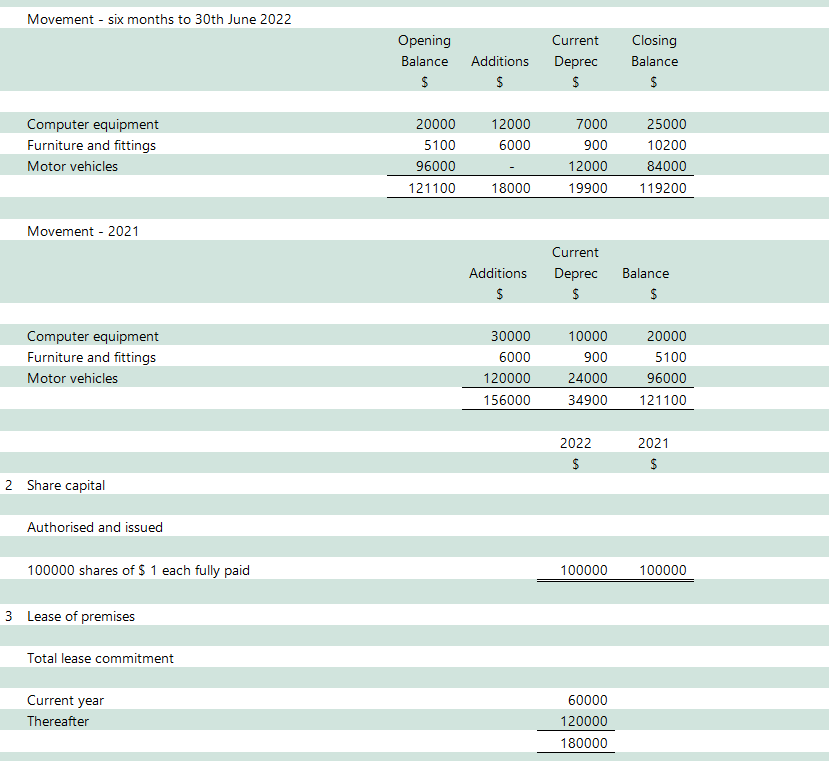

Depreciation summary spread sheet for six months

(additions bought on 1st January 2022)

The bank will want as much information as possible so there is no point in preparing minimum information management accounts. The bank will probably want personal guarantees from the sole shareholder and director. The director’s son has now been employed in the business. Training to take control should the incumbent sole director be incapacitated in any way. This is always a major consideration in respect of any loan advances and bank overdraft facilities being granted.

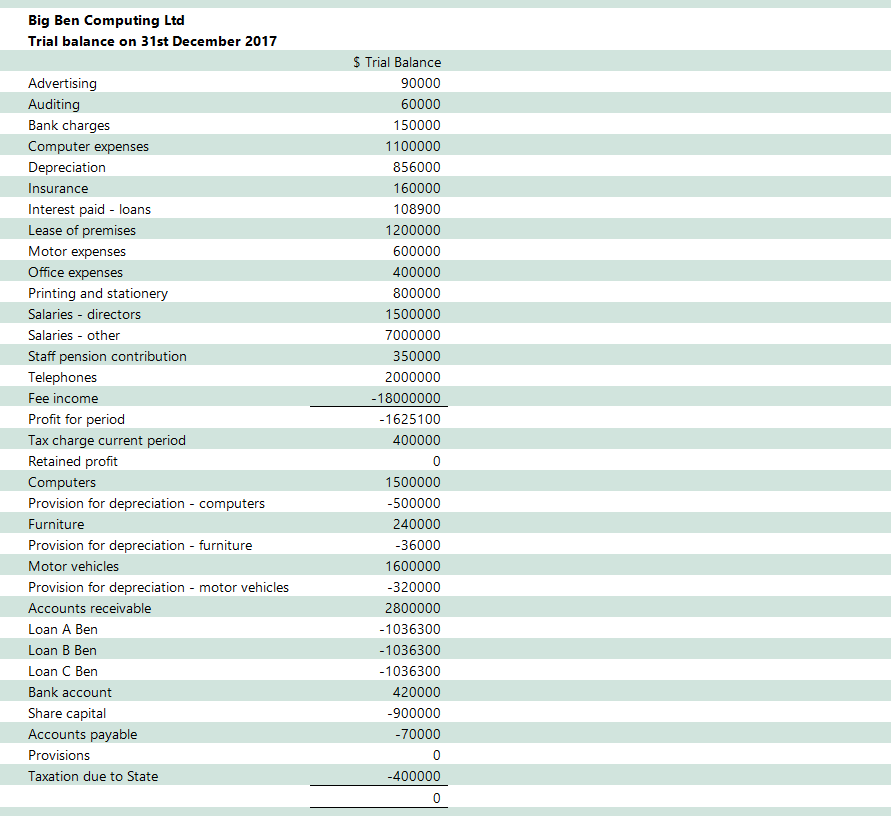

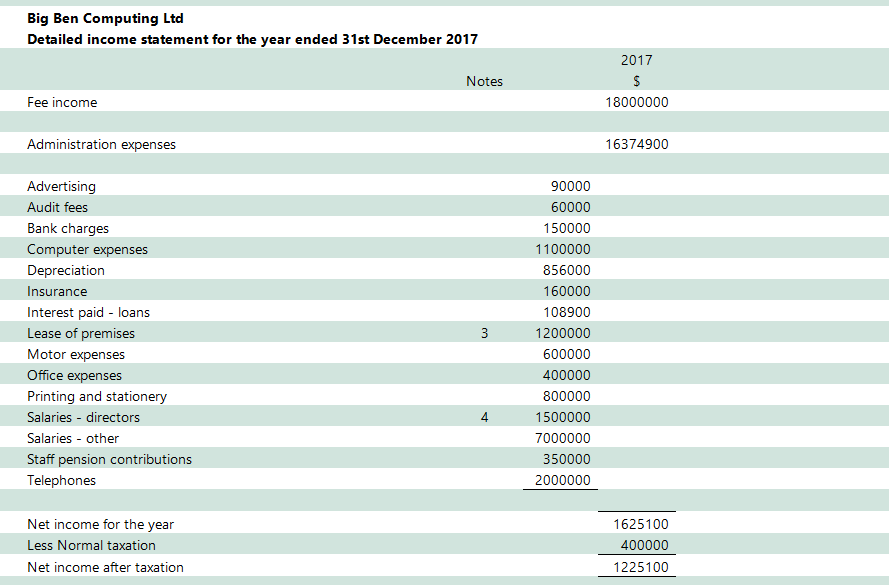

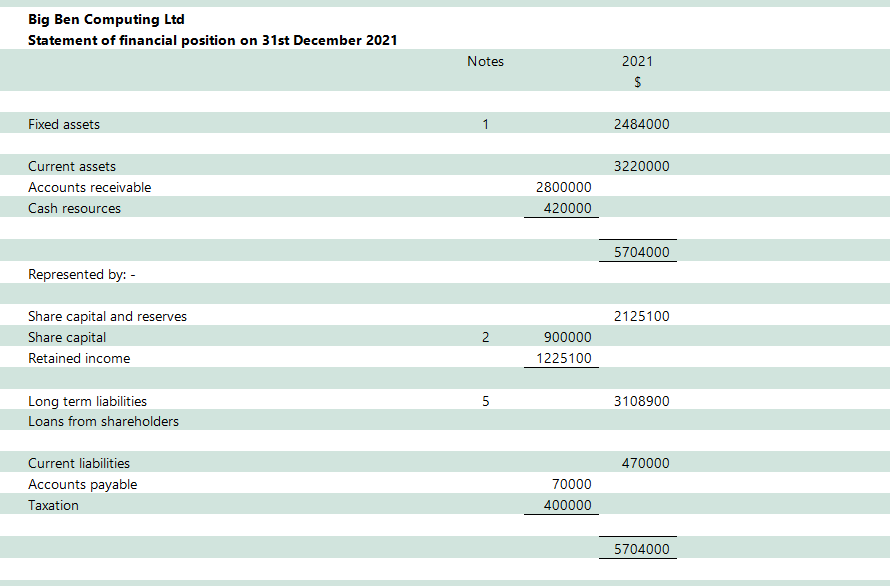

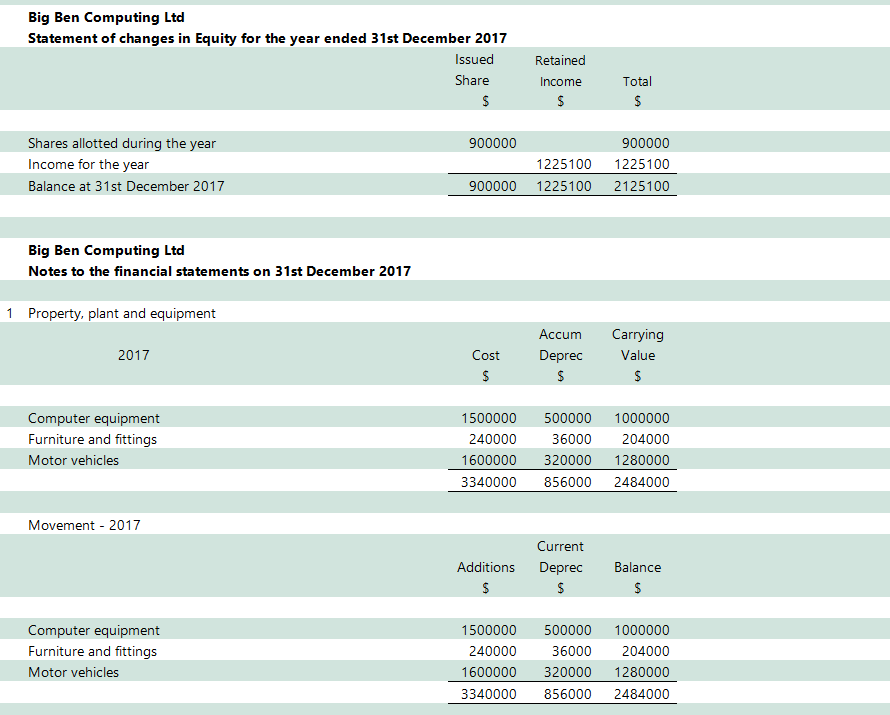

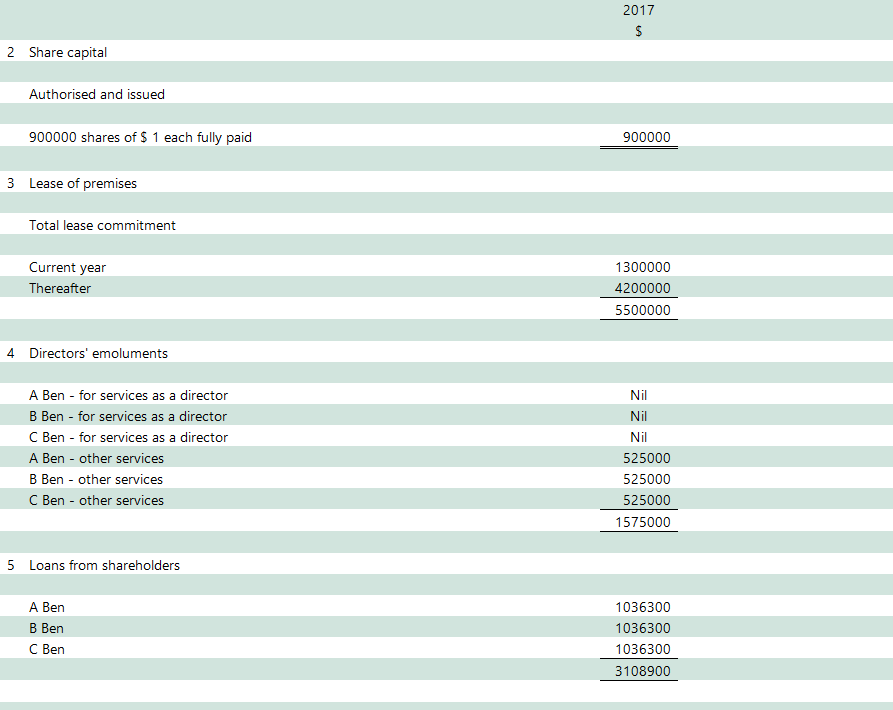

Example 3

Three brothers acquired an existing business from the deceased estate of the former employer of one of the brothers. They bought the fixed assets and the debtor book from the estate and no goodwill payment was involved. They formed their own limited liability company which commenced trading on 1st January 2017. This would be the first year of trading.

These loans are unsecured with no fixed terms of repayment and carry interest

at 3 % per annum.

The financial statements above are the basic disclosure statements which one would prepare. One then adds all the bells and whistles. The formal set of accounts would contain: –

1 Front page with details of company name, registered address, name of auditor,

names of directors and physical address of company.

2 Index

3 Audit report

4 Report of the directors

5 Statement of income and expenditure. This is the minimum disclosure version.

6 Statement of financial position

7 Statement of equity

8 Statement of cash flows

9 Notes to the financial statements (these usually run into a number of pages).

10 The detailed income statement